Bram Houghton

July 06, 2026

Economy Commentary Monthly update Monthly commentary

Market Update - July 2026

MARKET UPDATE: June 8th – July 3rd 2026

In a Nutshell: As negotiations continue in the Middle East, softening employment data out of the U.S. and weak GDP numbers in Canadian and European markets, central banks are left with some difficult decisions as rising inflations numbers loom. Despite this, solid earnings numbers continue in U.S. markets supporting company valuations amidst the geopolitical uncertainty.

Middle Eastern Conflict

The geopolitical landscape in June 2026 shifted decisively toward high-stakes diplomacy, culminating on June 17, 2026, when the U.S. and Iran signed a historic 14-point Islamabad Memorandum of Understanding. This framework established an extendable 60-day ceasefire window to negotiate permanent terms, lift blockades, and reopen the Strait of Hormuz. Despite a follow-up Israel-Lebanon security meeting in Washington on June 22, the truce remains intensely fragile; with drone strikes continuing in the conflict area.

Outlook: Near-term stability hangs entirely on the 60-day negotiating window; if political or military cross-border frictions disrupt the talks, the fragile truce will dissolve, immediately plunging shipping corridors back into active conflict and triggering severe energy supply shocks.

U.S. Labour Markets

The job market showed sharp cooling as the Bureau of Labor Statistics reported on July 2, 2026, that June nonfarm payrolls added a meager 57,000 jobs, far below expectations of 110,000. Compounding this, downward revisions to April and May slashed a combined 74,000 jobs from previous tallies, while private payrolls grew by just 49,000 positions and leisure and hospitality shed 61,000 jobs. Despite weaker hiring, the headline unemployment rate dipped to 4.2% due to a massive contraction in the labor force, while initial jobless claims for the week ending June 27 held flat at 215,000 and annual nominal wage growth tracked steadily at 3.5%.

Outlook: The dramatic slowdown in payroll expansion indicates that the labor market is entering a highly vulnerable, low-utilization phase; while mass layoffs remain absent, a shrinking hiring margin leaves employment increasingly exposed to sudden macroeconomic shifts.

U.S. Economy

The broader economy displayed a resilient but stubborn inflationary profile as Q1 2026 real GDP expanded at an annualized 2.0% rate. However, underlying cost pressures mounted as headline CPI inflation climbed to 4.2% year-over-year due to high energy costs, while core PCE inflation printed at 3.3%. Manufacturing activity managed to hold expansionary territory with the ISM Manufacturing PMI printing at 53.3, but persistent inflation prompted the Federal Reserve to maintain the benchmark interest rate target at 3.50%–3.75% at its June meeting, subsequently pushing weekly mortgage rates up to 6.52%.

Outlook: Sticky inflation will force the Fed to maintain a restrictive 3.50%–3.75% interest rate range deep into the second half of 2026, which will eventually act as a major headwind for corporate expenditures and late-year consumer discretionary spending.

Canadian Economy

Canada's economic momentum faced severe domestic headwinds, confirmed by national accounts showing real GDP completely stalled at 0.0% for the first quarter of 2026. Stagnant growth was primarily dragged down by a 0.7% drop in business capital investment and a 2.9% surge in imports, even though full-year forecasts expect a modest stabilization to average 0.8% to 1.1% growth. Headline CPI hovered near 2.8% to 3.0% due to elevated energy inputs, forcing the Bank of Canada to signal a prolonged pause on its policy rate at 2.25% while real retail sales volumes contracted.

Outlook: Canada faces a sluggish, multi-track near-term expansion as households grapple with high domestic energy costs and ongoing structural adjustments to U.S. tariffs, leaving any late-2026 recovery heavily dependent on global oil prices easing.

Eurozone and UK Economy

The European economic arena highlighted a clear multi-track performance over the past month. In the Eurozone, factory expansion slowed as the flash S&P Global Manufacturing PMI hit a 3-month low of 51.4, while inflation diverged with Germany’s headline CPI ticking up to 2.9% and France easing to 2.5%. Conversely, the United Kingdom outpaced its continental peers with Q1 GDP expanding by a stronger-than-expected 0.6% quarter-on-quarter, prompting the IMF to lift its full-year 2026 UK growth outlook to 1.0% as British CPI inflation fell to 2.8%.

Outlook: While the UK maintains a temporary growth and disinflation edge over a decelerating Eurozone, both regions share massive stagflationary risks heading into the summer; upcoming domestic energy price cap hikes and lingering maritime supply disruptions are expected to compress industrial margins and push regional CPI back toward the **3.5% range** by year-end.

Asia and Far East

East Asian economic indicators continued to reveal a deep structural divide. In Japan, the 10-year government bond yield spiked to 1.08% (its highest since 2011), forcing the BOJ to signal policy interventions to defend the yen near the sensitive 160 level against the USD, despite national CPI forecasts targeted at 2.9%. Meanwhile, China’s industrial complex was bolstered by Beijing's 2.4 trillion Yuan infrastructure stimulus package, pushing its Manufacturing PMI to 51.4. However, domestic consumer sentiment collapsed, sending retail sales growth to a 4-year low of 0.2% due to a 15.3% plunge in automobile sales.

Outlook: East Asia remains locked in an uneven, policy-dependent recovery; Japan is navigating a structural shift toward a mid-year interest rate hike to combat currency depreciation and absorb historic wage gains, while China remains a starkly divided economy where aggressive state capital injections prop up factory production but fail to break deep-seated domestic real estate and consumer anxiety.

Commodities

Energy and precious metals markets moved through a significant consolidation phase over the last four weeks as geopolitical risk premiums deflated. Global crude prices trended down toward one-month lows, leaving WTI crude trading near $87 per barrel and Brent crude near $92 per barrel. The U.S. EIA reported that commercial crude oil reserves dropped significantly by 8.0 million barrels to 433.7 million barrels (roughly 3% below their five-year historical average). Conversely, natural gas storage expanded with an 85 Bcf weekly injection, keeping a comfortable 140 Bcf surplus. In precious metals, gold experienced a cooling-off period following its historic multi-month run, with COMEX futures closing just under $4,490 per ounce.

Outlook: Low commercial stockpiles leave crude oil highly vulnerable to supply-side shocks, meaning any sudden collapse in regional peace negotiations could instantly trigger inventory depletion and spike oil back over $100 per barrel. For gas, North American regional surpluses will mask global supply tightness from damaged Middle Eastern infrastructure, which will prolong tight market conditions into 2027. For gold, the minor pullback represents a temporary consolidation phase before central bank accumulation and structural inflation hedges drive long-term targets toward $5,400 to $6,000 per ounce by late 2026.

Latest Equity Market Data

| Market Data | S&P/TSX | S&P 500 | DOW | NASDAQ | STOXX EU | WTI | GOLD |

| This Week | 1.2% | 1.7% | 1.9% | 1.9% | 1.6% | 65.0% | 2.7% |

| Last Month | 1.4% | -1.7% | 3.1% | -4.7% | 3.4% | -28.4% | -5.6% |

Reuters Market Updates http://www.reuters.com

Bloomberg Market Updates - https://www.bnnbloomberg.ca/markets

The Earnings Engine: How Brian Belski's 2026 Thesis Is Playing Out by AdvisorAnalyst.com Editorial Team Link to article & Sources

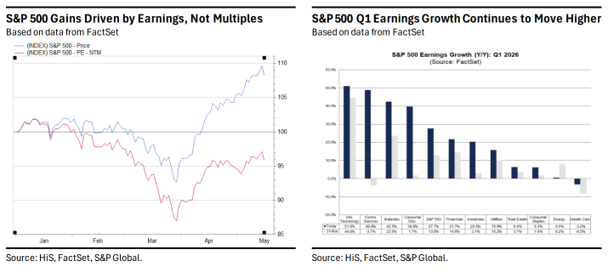

Brian Belski of Humilis Investment Strategies thesis for 2026 is playing out largely as expected: this is an earnings-driven market, not one propped up by investor sentiment or expanding valuations. That distinction matters, because it means gains are being genuinely earned. Q1 2026 earnings growth came in at a remarkable 28.4%, more than double the 13% originally anticipated — with 84% of S&P 500 companies beating expectations. Notably, the S&P 500 is up roughly 8% year-to-date while the forward price-to-earnings ratio has actually contracted, confirming that earnings, not enthusiasm, are doing the heavy lifting.

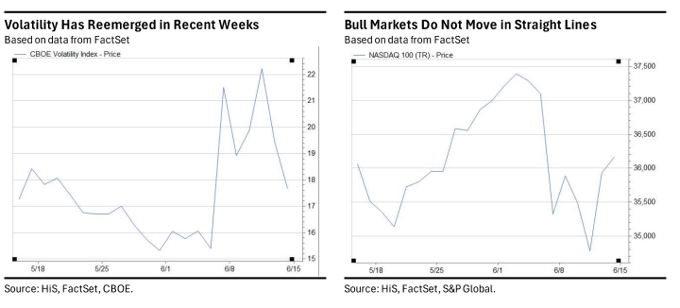

The flipside of an earnings-driven market is that it tends to be bumpier than one fueled by optimism alone which is what investors have experienced in 2026. Following a sharp 12–15% recovery after the Middle East ceasefire, markets gave back some gains. Belski's team views each of these pullbacks as a healthy reset and a potential entry point rather than a reason for concern. The base case remains constructive — volatility is expected to persist as markets remain sensitive to geopolitical headlines and AI capital spending developments, but the underlying earnings story continues to support a higher market through the second half of 2026.

MacroMemo - June 16- July 6, 2026 by E.Lascelles, J.Nye Link to Article

U.S. Economic Resilience

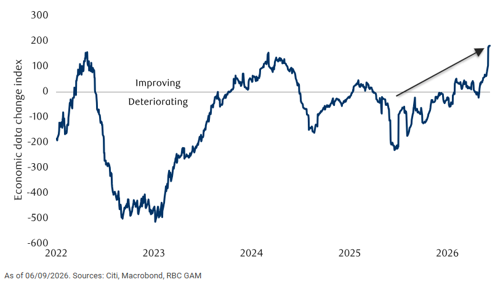

The U.S. economy remains on solid footing despite global energy pressures, with Citi's U.S. Data Change Index now at its highest level since 2021. The labour market is healthy, job gains are averaging 114,000 per month which is well above demographic trends, and job openings once again exceed the number of unemployed persons. Business investment, particularly in technology, continues to surge, with the top five hyperscalers expected to spend $738 billion this year. Leading indicators like the ISM surveys are firmly in expansionary territory, and the Atlanta Fed is tracking a strong 3.3% annualized GDP growth in Q2. Our outlook remains above consensus, forecasting 2.2% growth for 2026, supported by AI capital expenditure, stock market wealth effects, and tax cuts.

U.S. economic data is generally improving

What’s driving U.S. productivity growth?

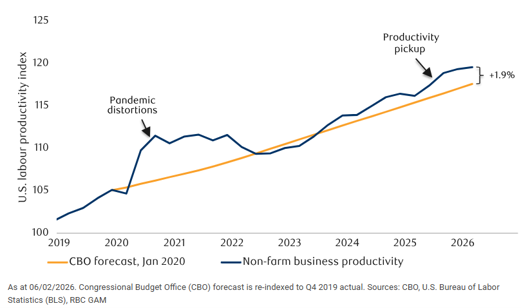

U.S. labour productivity is growing at nearly 3% year-over-year — its fastest pace in two decades outside of post-recession rebounds. AI appears to be a meaningful, though not the only contributor. Studies suggest AI adoption has boosted productivity by around 1.3% since ChatGPT launched in late 2022, and industries with higher AI adoption are generally seeing stronger productivity growth. Broader technology investment, the gradual unwinding of post-pandemic over-hiring, and workforce composition shifts are also playing supporting roles. Looking ahead, AI is expected to become an increasingly powerful driver of productivity gains as adoption rises and models mature, with benefits set to extend well beyond the U.S. to businesses and investors around the world.

U.S. labour productivity growth has outperformed expectations

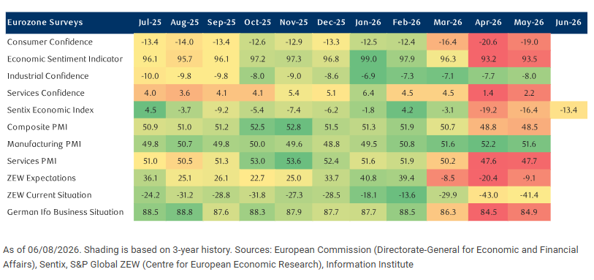

European Recession Risk

The Eurozone economy contracted by 0.2% in Q1, its first decline in 10 quarters, raising the possibility of a technical recession if Q2 follows suit. However, context matters as the decline was heavily distorted by a record 12% drop in Irish GDP, driven by multinational accounting quirks rather than true economic weakness. In fact, Germany, Italy, and Spain all posted solid growth in Q1, suggesting the underlying Eurozone economy was healthier than the headline number implies.

Q2 presents more genuine challenges, as Europe is more exposed to the energy shock than North America given its status as an energy importer. Assuming the Strait of Hormuz reopens, and energy prices don't rise significantly further, economic downturn can likely be avoided, and a potential reversal of the Irish GDP distortion could help Europe sidestep a technical recession altogether.

Most recent Eurozone surveys showed tentative signs of stabilization

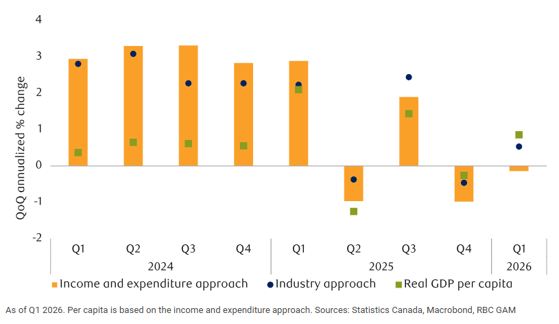

Is Canada in a Recession?

Despite two consecutive quarters of slight GDP contraction, technically meeting one definition of a recession. RBC Gam does not believe Canada's economy is truly in one. The Q1 decline of 0.1% is within the margin of error, and a separate industry-based measure actually shows growth of 0.5%. More importantly, the economy expanded on a per-capita basis, unemployment has been declining, consumer spending held up, and StatCan's flash estimate for April points to a solid 0.4% rebound — the strongest reading in nine months.

However, the economy isn't firing on all cylinders. Unemployment remains elevated, growth has become increasingly reliant on government spending, and slower population growth has lowered the country's speed limit for GDP expansion. However, there are reasons for cautious optimism — business and consumer confidence are improving, higher oil prices are supporting exports, and housing is showing early signs of stabilization.

Canadian GDP increased on a per capita and industry basis in Q1

If you think others may benefit from reading our content, please don’t hesitate to share it with them.

Aurie Wicks, CA, CPA, CFP® Tyler Quinn, CIM®, FCSI Bram Houghton, CFA, CFP®

Wealth Advisor Sr. Investment Advisor, Associate Portfolio Manager,

(403) 835 - 4785 Portfolio Manager Wealth Advisor

aurie.wicks@cibc.com (403) 299 - 7356 (403) 260 - 0597

tyler.quinn@cibc.com bram.houghton@cibc.com

Related posts

Bram Houghton

October 14, 2025

Market Update - September 8th - October 10th, 2025

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read moreBram Houghton

September 10, 2025

Market Update - August 2025 Edition

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read more