Julian Hoyle

October 08, 2021

Economy Commentary Quarterly update Quarterly commentary

Rising Rates and Hovering Bids

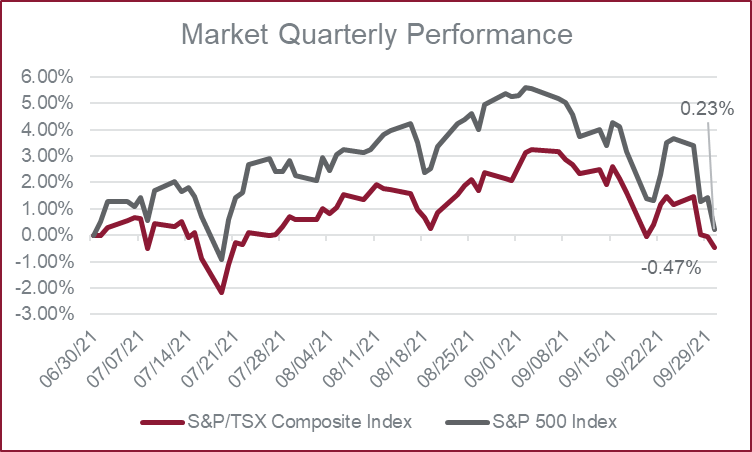

The third quarter of any year comprises the summer months here in North America. These months normally lead to traders and investors on vacations, which often take a lot of the air out of whatever trend was previously prevailing. This summer was no exception, with the strong results we had seen thus far this year puttering out, and then struggling along as we reached September, and the stock market slump that came with it. On the quarter, the S&P/TSX Composite closed down -0.47%, while the S&P 500 was slightly up 0.23%.

While some of this can be attributed to the simple explanation above, there were certainly other factors at hand. As we discussed last quarter, inflation has been a hot topic issue for nearly half a year now. The large fiscal stimulus imparted by federal governments in Canada and the US during the height of the COIVD-19 Pandemic led many to believe prices were sure to increase. Sure enough we have seen a rise in both the CPI and the short term yield curves over the quarter. While rates are likely to push higher in the future as governments reload their "recession rate cut gun", CPI rates may well be more transitory.

Oil in particular has been on a tear as of late. WTI Futures closed the quarter at $75.03 per barrel, up 4.14% on the quarter and 58.56% on the year. OPEC has continued their line of gradual supply increases, even in the face of rising prices. This is slated to continue, with Canadian energy names already seeing a benefit.

A final note must be had on the recent Canadian election. Through much posturing, nothing in particular has changed, with the Liberals picking up only a couple seats, and confirming their slim margin to govern. We don't expect this minority government will fall before the end of term, and Justin Trudeau and the Liberals should be able to make minor adjustments without rocking the boat too much. We stay tuned to all messaging in advance of the next budget.

Figure 1 Sourced from Thomson one

Figure 2 sourced from Bank of Canada