Prepared by: Gale Wealth Advisors

May 21, 2026

Education Economy Commentary In the news News Trending

Japan's Bond Market Is Breaking

The world is no stranger to a debt crisis. From Latin America in the 1980s to the Asian Financial Crisis of the late 1990s, sovereign debt blowups have been a recurring feature of global markets for decades. What used to be confined to emerging markets has crept steadily into the developed world. The Eurozone crisis, the U.K. gilt crisis of 2022, France's snap election sending sovereign spreads to their widest levels in over a decade; the pattern is consistent. Political risk and fiscal irresponsibility get punished, and no country is immune. But what is unfolding in Japan today is structurally different from every prior episode, and the consequences are global.

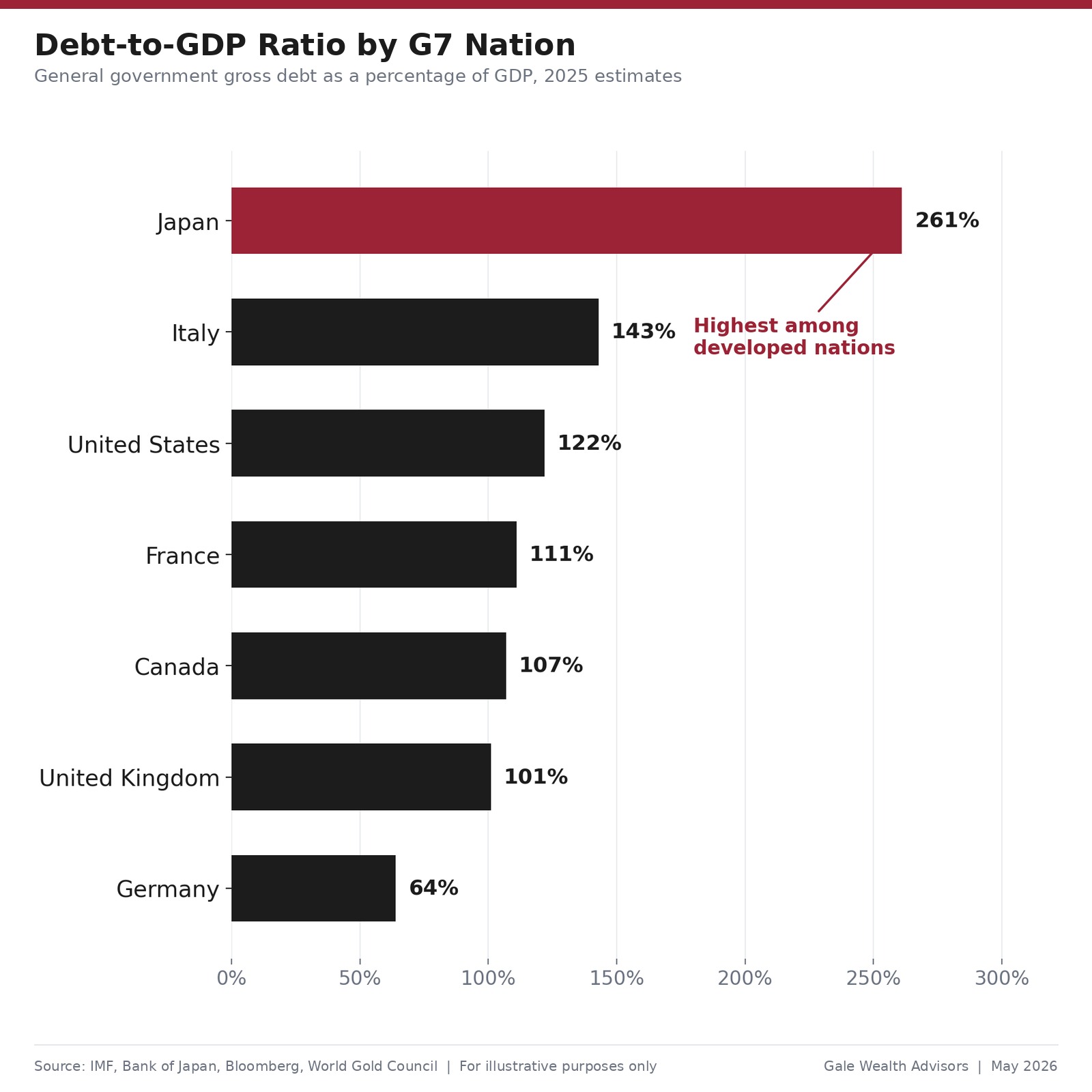

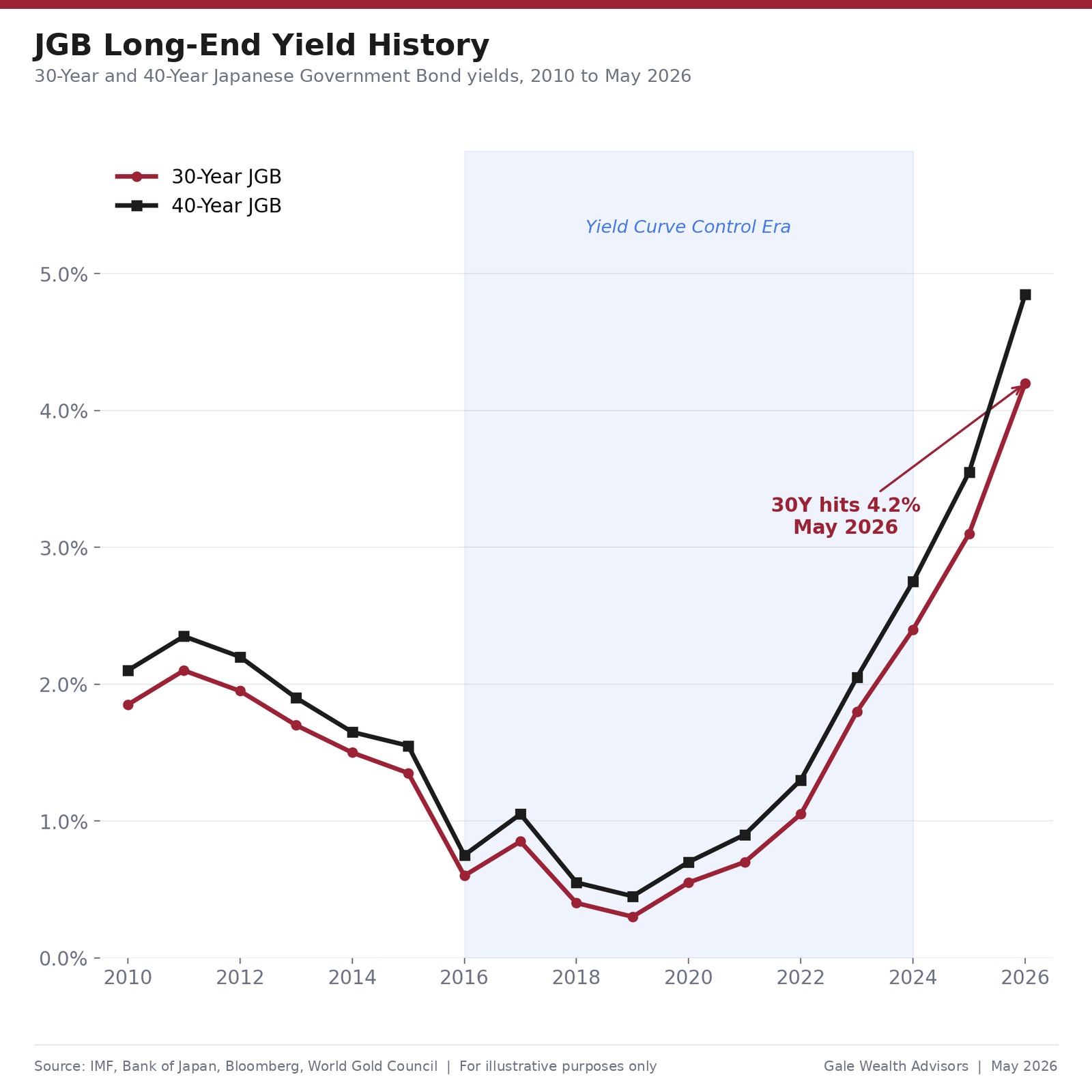

For three decades, the Bank of Japan (BOJ) suppressed borrowing costs at near-zero rates through Yield Curve Control, allowing Japan to carry a debt-to-GDP ratio exceeding 260%, the highest among developed nations, without triggering a funding crisis. And that suppression is beginning to collapse. The 30-year Japanese Government Bond (JGB) surpassed 4% for the first time since its creation in 1999, reaching 4.2% in May 2026, while the 40-year bond has pushed to unprecedented multi-decade highs. Past debt scares were repricing events: sharp, painful, but ultimately contained. What Japan is facing now is the dismantling of a structural foundation that has been thirty years in the making, and there is no obvious 'exit door' in sight.

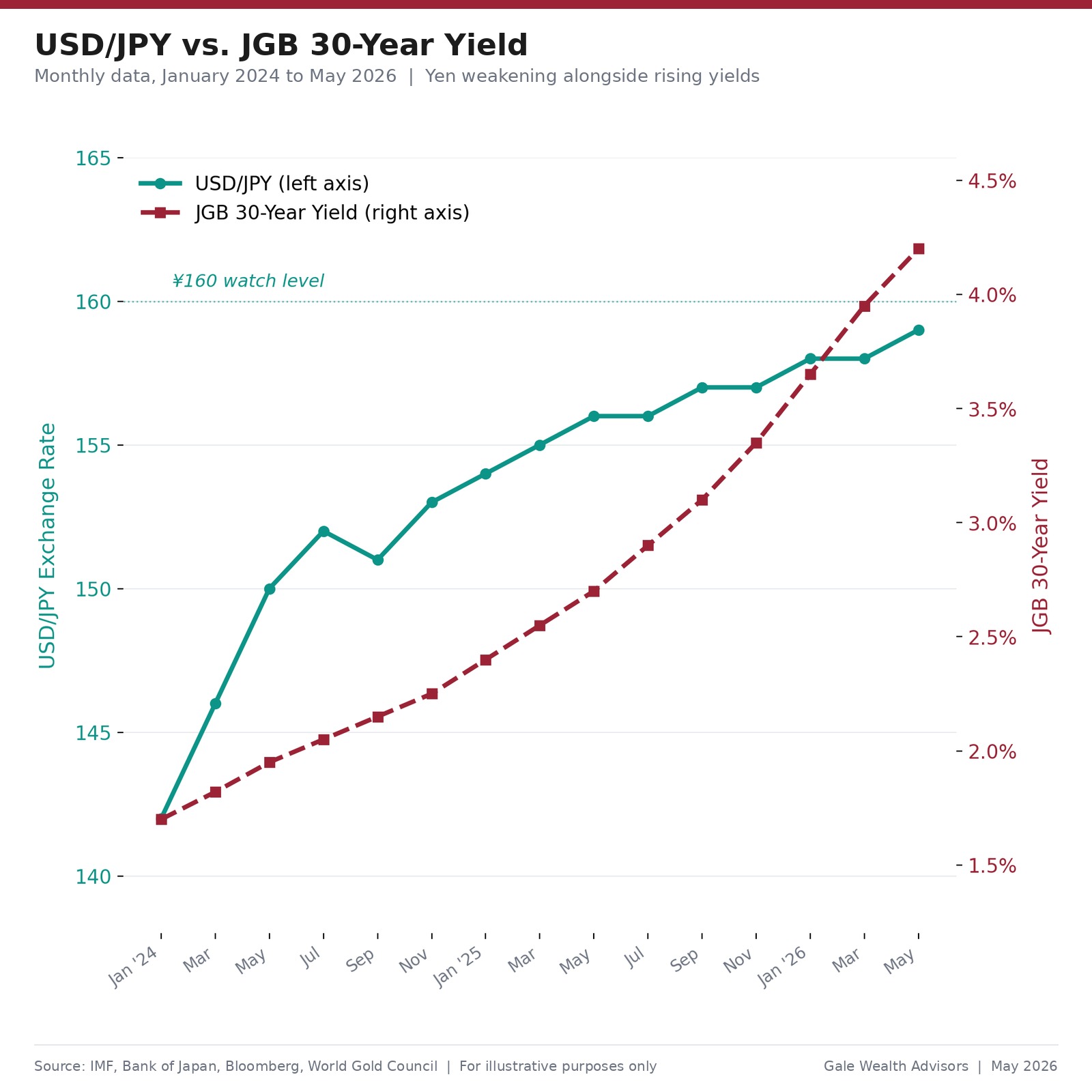

Japan is caught in a bind with no clean exit. If the BOJ raises interest rates to defend the collapsing yen, the government's interest payments on its debt explode. If it keeps rates low to manage the debt burden, the yen plummets, triggering domestic inflation and capital flight. Prime Minister Takaichi's push for fiscal stimulus, tax cuts, and a snap lower-house election has only worsened the situation, compressing into four days the same bond spread widening that took France six months after its own snap election. The yen has been weakening toward 160 per US dollar, and Japan holds roughly 1.4 trillion dollars in foreign-exchange reserves, much of it in U.S. Treasuries. If those holdings are sold to defend the currency, U.S. yields rise, mortgages rise, credit becomes more expensive, and the stress on Japanese bonds becomes stress on American bonds. The 30-year U.S. Treasury reached 5% as these pressures were building and it's creating a domino affect where the biggest pieces fall on our side of the pond.

What separates this episode most sharply from prior JGB scares is the collapse of the domestic buyer base. In past episodes, life insurers, major banks, and the BOJ itself provided a reliable floor for JGB demand. That floor is gone. Domestic institutions have turned into aggressive sellers, creating the worst liquidity conditions in JGB history. Japanese investors sold close to 29.6 billion dollars in U.S. debt in the first quarter of 2026 alone, the largest quarterly sale since 2022, as capital repatriation accelerates. The Iran conflict is compounding all of this, with Brent crude remaining more than 50% above pre-war levels and average G7 10-year borrowing costs climbing toward 4%, compared with roughly 3.2% before the conflict began. The conditions that made Japan's debt manageable for thirty years, near-zero rates, a captive domestic buyer base, and a stable yen, are all deteriorating simultaneously.

Three indicators are worth watching closely: the USD/JPY exchange rate near 160, U.S. 10-year Treasury yields, and official commentary from Japan's Finance Ministry. The patterns of the past are visible in the present, but this time, the structural foundation underneath those patterns looks meaningfully different.

Related posts

Spencer Onslow

May 11, 2026

CUSMA: Prepare for the Headlines, Don't Trade on Them.

Despite the headlines, the Carney-Trump relationship is stronger than it appears, and CUSMA is in better shape than consensus reflects.

Read moreSpencer Onslow

May 14, 2026

Taiwan and AI: The Real Stakes in Beijing This Week

Beijing sees a clear opening to extract a compromise from an administration that has already signaled hesitation on both fronts.

Read more