Jay Smith & Brad Brown

November 01, 2025

Monthly commentary

November 2025

MONTHLY MARKET MUSINGS

November 2025

Steady As She Goes

Both the U.S. Federal Reserve (Fed) and the Bank of Canada (BoC) kept cutting rates in October. Whether we see a continuation of cuts into December seems a bit cloudier than it was previously. On the Canadian side of things, the BoC seemed to suggest that the rate cutting cycle may be done for 2025 and that any additional cuts will be determined by the pace of growth and the overall health of the Canadian economy. The hope for the BoC is that the economy continues at a controlled pace of modest growth and that inflation remains in check, near the central bank's 2% target rate. Any weakness in the economy would likely be followed by renewed rate cuts and any unexpected spike in inflation would likely be followed by a more extended pause. So, we are currently in the wait-and-see period where data will be dictating the central bank's next move. As for the Fed, the chance of a cut in December has also diminished slightly as the U.S. central bank is not seeing unanimous data supporting another one just yet. The market still seems to have a slightly higher expectation for another cut before the year is done. Similar to Canada, the data in the next two months will likely drive much of the decision and if the U.S. sees increased costs stemming from the tariffs begin to take shape in the prices of goods and services, it would check another box in favour of a pause into year-end.

Earnings season has kicked off and one of the biggest takeaways thus far has been that there is no slowdown in capital expenditures (capex) for technology firms. In fact, many have increased their projected spending on AI for 2026. [1] Some estimates have noted that the largest technology firms are going to spend US$550B in 2026 on AI.[2] The big question that many continue to ask is whether all of this spending from these tech companies will equate to higher earnings. While it is safe to say that some of the investments will end up being a sunk cost and will not develop into anything, the large technology firms have already begun to monetize some of their efforts by integrating the first wave of AI products into their software subscriptions. This provides customers with more features and allows them to optimize their productivity and thus justifies an increase in annual subscription fees. This is one of the reasons why many say the AI revolution is different than the dot.com era. The path to monetization of a concept/product has already been defined and access to end users has already been established. There is no timely distribution buildout required like there was back in 1999/2000, in this case, the product can be quickly delivered to customers and the additional revenue generated. For many end users of these enhancements, the increased cost seems like an immediate financial burden but ultimately, if it creates efficiencies and results in increased productivity then that should justify the expense. Will a 20-30% increase in software subscription prices offset the capex spent on AI, maybe not at first. But eventually, having integrated AI built directly into products and services will become commonplace and be a necessity for most businesses in order to remain competitive.

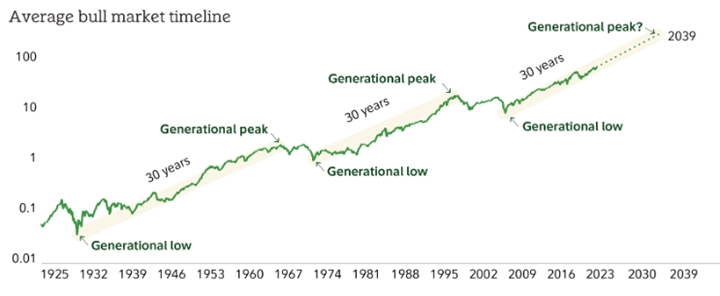

While the tech sector keeps us positive on equities in the near term, overall, we continue to see upside within the current cyclical bull market which started back in 2022. Given that the average cyclical bull market lasts nearly 5 years, it would suggest that there is still some legs to this market in the coming years before we see another potential correction.[3] If we look at the even longer term trends or in this case, the secular bull markets, we have many more years to go. According to Fidelity, secular bull markets last approximately 30 years from a generational low to a generational peak.[4] We have seen this pattern repeat itself several times over the past one hundred years with the most recent generational low having been shaped during the 2008-2009 Financial Crisis. This suggests that the current secular bull market could potentially continue up until 2039 if we continue along the same historical pattern. Of course, this does not mean that there will not be corrections along the way. That is where the cyclical bear markets play out. A secular bear market, however, where a generational peak is achieved just prior to it starting, could possibly still be relatively far away if this trend continues to hold true.

Source: https://www.fidelity.com/learning-center/trading-investing/why-the-bull-market-may-have-years-to-run

[1] https://www.cnbc.com/2025/10/31/tech-ai-google-meta-amazon-microsoft-spend.html

[2] https://www.cnbc.com/2025/10/31/big-tech-ai-spending-billions-microsoft-google-software-subscriptions.html

[3] https://www.reuters.com/business/wall-streets-bull-market-nears-three-years-old-history-shows-it-may-still-have-2025-10-09/

[4] https://www.fidelity.com/learning-center/trading-investing/why-the-bull-market-may-have-years-to-run