Andrew Pyle

September 09, 2022

Comparisons to crisis not valid, at least not yet

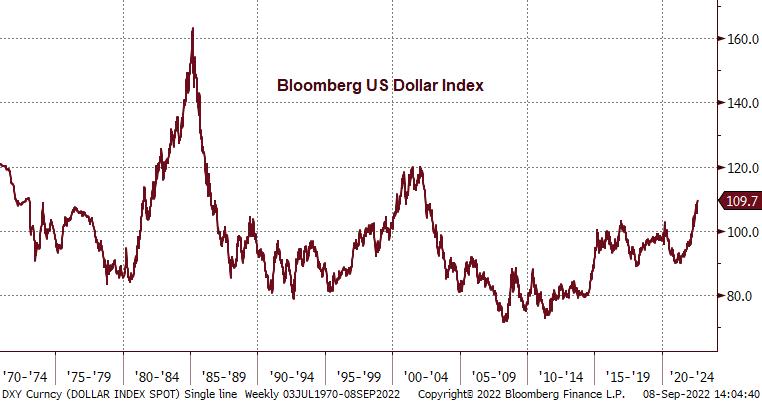

As much as investors have been laser-focused on inflation and rising interest rates these past months, something else is about to completely overshadow these issues and that is the strength of the US dollar. From last summer, the Bloomberg DXY dollar index has climbed by close to 23% to a high of just over 110. This is the best level the index has reached since June 2002, which was after the dollar index had topped out around 120.

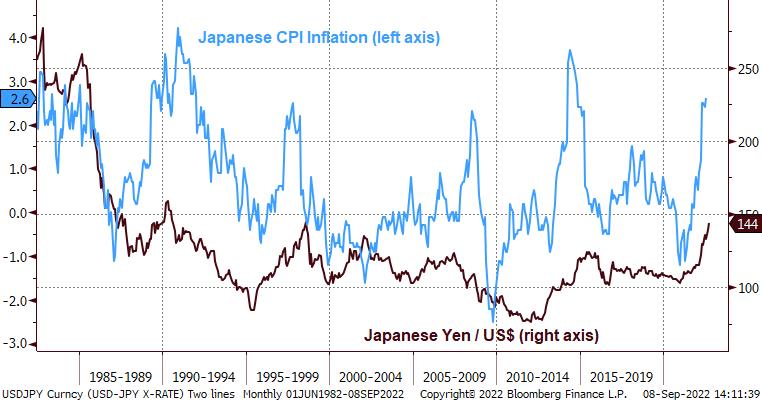

While our Loonie has continued to sink, despite the Bank of Canada hiking its overnight rate target by 0.75% this week, the major brunt of the dollar’s climb is being felt in Europe and Asia. Pound sterling and the euro are down by 15% and 12%, respectively since the start of the year, while the Japanese yen has tumbled by 20%. Other emerging markets have performed even worse, such as the Venezuela (down 42%), Argentina and Turkey (both down 27%). The decline in the value of the Yen to a level of over 140 yen to the dollar is notable as it is weakest the currency has been since 1998. This has led some to make comparisons with the Russian financial crisis of 1997 and the Asian Contagion of 1998.

It is true that the relentless surge in the American greenback is placing undue pressure on many countries around the world. Europe is already likely in a recession as it deals with not only the war in Ukraine but the related spike in energy prices. The new British PM has already announced a government support package of 170 billion pounds to relieve consumers and businesses. At the same time, central banks in Europe are being forced to tighten monetary policy aggressively to combat soaring inflation, even though these rate hikes will only exacerbate weakness in the economy. At the same time, the depreciation in both the pound and euro will add to inflationary pressures as the cost of imported items goes up.

It's important to note that it wasn’t that long ago when investors were fretting about the gargantuan amount of bonds that had negative interest rates. The ECB’s deposit facility rate was taken below zero back in 2014 and it stayed there until this past July, when it was hiked half a percent back to zero. This Thursday, the key rate was moved up by three-quarters of a point to 0.75% - a return to 2011. If there is no real progress on inflation, economists expect the rate to move even higher. Denmark, which was the first country to experiment with negative interest rates, also hike its official rate by the same amount, taking it to 0.65%.

Japan has so far resisted the drive to higher interest rates (the official rate remains at minus 0.1%), mainly because it doesn’t see the same inflation concerns as the other G7 nations. Inflation has pushed up to 2.6% this summer but remains below the 3.7% high in 2014 which was the loftiest it had been since 1990. If anything, Japan has struggled over the last forty year to keep inflation even in positive territory. The moving average over this period is only 0.7%, or two percentage points below the average for the US. That said, officials in Japan called a meeting this week to deal with the ever-falling yen.

Still, this is not anything close to what the world went through in 1997-98. In 1998, Thailand initiated a wave that ultimately became an Asian crisis after it unpegged its currency from the US dollar. The rationale for the decision was that a stronger dollar was making Thailand and other countries with dollar pegs hugely uncompetitive in the export arena. Unfortunately, the decision led to a massive devaluation and capital outflows. Global markets were shaken, and the IMF was forced to step forward in an attempt to stabilize conditions.

Keep in mind that the Fed had just come off a very aggressive tightening cycle in 1994-95 and, even though it started to cut rates into 1996, it adjusted them up a notch in the first half of 1997. I’m not saying that the last hike was a misstep, but it contributed to dollar strength. Following the Asian crisis, Russia then experienced a debt crisis in 1998, as it was unable to make payments on ruble-denominated debt, but also debt that was priced in US dollars. This past July, Russia was said to be in technical default. Unlike 1998, this was not because of a lack of funds, but because a lack of access to US dollar funds because of sanctions linked to the Ukraine invasion. The Russian ruble has lost close to 60% of its value since before the invasion, which took inflation in the country to almost 18% in the second quarter. With an economy in recession and inflation this high, Russia is about as close to a crisis as you can get.

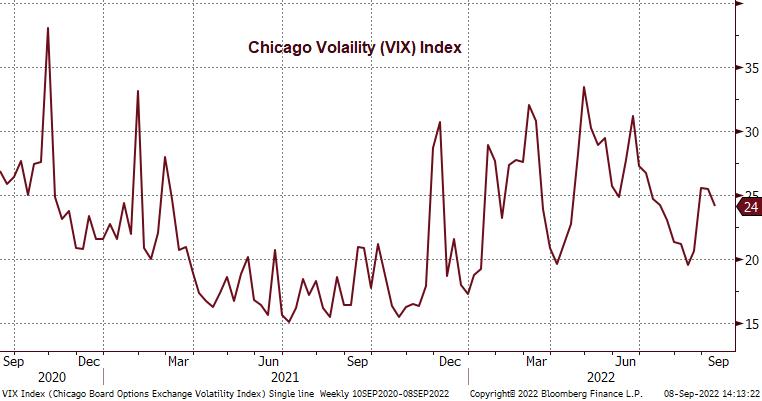

However, world markets are not behaving like we are on the doorstep of crisis. True, most equity markets are still in correction territory this year, but volatility is actually down from what we saw in the second quarter. There is also not a flood of investments into the safe haven of government bonds, which is what we saw in 1998. Since there is no crisis, the Fed and other central banks still see room to lift interest rates, which makes it hard for bonds to rally. The 10yr US yield has climbed back to 3.3% after falling from almost a percent form its peak near 3.5% in June – clearly not the sign of crisis behaviour.

It's important for investors to not get caught up in the daily headlines and commentaries, but to focus on what the fundamentals are telling us. At this stage, we are still in the middle of a tightening phase by an increasing number of central banks. As long as the Fed keeps raising rates (we expect a 0.75% move on September 21st) and other economies are weaker than the US, then the greenback will probably continue to appreciate. Assuming that inflation is truly on the decline, I believe that we are getting close to the end of this rate cycle and that might mean the US dollar can fade as well. This would take pressure off developed and developing economies and help protect against a 1997-98 crisis from emerging. It does not mean that we are guaranteed to avoid one. That will depend on careful the Fed will be in the coming months, and it might even depend on the major central banks intervening to lower the dollar’s value. Stay tuned.

Have a great weekend everyone

Andrew Pyle

CIBC Private Wealth consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc. “CIBC Private Wealth” is a registered trademark of CIBC, used under license. “Wood Gundy” is a registered trademark of CIBC World Markets Inc. This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2022.CIBC Wood Gundy, a division of CIBC World Markets Inc.

These are the personal opinions of Andrew Pyle and the Pyle Group and may not necessarily reflect those of CIBC World

Related posts

Andrew Pyle

June 17, 2022

Market volatility underscores the need for advice

This week's events have led to confusion among investors and apparently policy-makers too. Even though the economy is cooling off, markets are still fixated on mega rate hikes. This has led to selling...

Read moreAndrew Pyle

June 15, 2022

Fed damns the torpedoes with 0.75% hike

The Federal Reserve did something it hasn't done since 1994 and that was to increase rates by three-quarters of a point. This was anticipated by the market and shows that the Fed is even more serious ...

Read more