Andrew Pyle

September 16, 2022

Prognosis for oil not great, but maybe not a disaster either

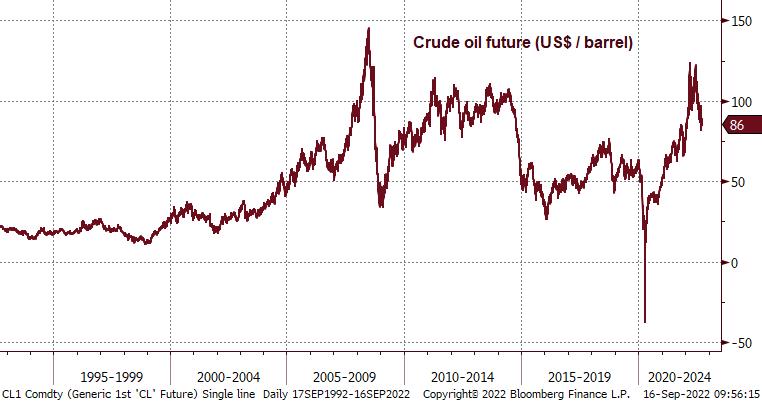

It doesn’t seem that long ago that crude oil prices were trading sharply higher than $100 per barrel and analysts were throwing around all sorts of wild forecasts, like $160 or even $300. The post-pandemic world, made stranger by the invasion of Ukraine, was going to introduce such supply distortions that crude prices would resist decline. Even though the global pivot to clean energy was not going to reverse, meaning long-term demand for oil consumption growth would diminish, producers would be even less incentivized to invest capital in operations, thus reinforcing supply constraints. The same would hold true for gasoline refineries.

Today, those same concerns about supply are lingering, but the bullish forecasts of the second quarter have been pushed aside in the face of recession talk. Last week, the first contract on West Texas Intermediate (WTI) futures fell to just above $81 – reversing all of the progress made from early in January to its intraday peak of $130 in March.

A modest recovery was again cut short on Thursday when the White House said that there was no price target for replenishing the US strategic oil reserves. Recall that when prices were soaring and pocketbooks were being emptied at gas pumps across the US, President Biden initiated a sizable release of reserves to improve supply conditions. Since it costs money to re-stock those reserves, the market’s belief was that this recent drop in prices would see the Administration step in start buying. The announcement turned that view on its head and resulted in a drop of more than three dollars at the close on Thursday.

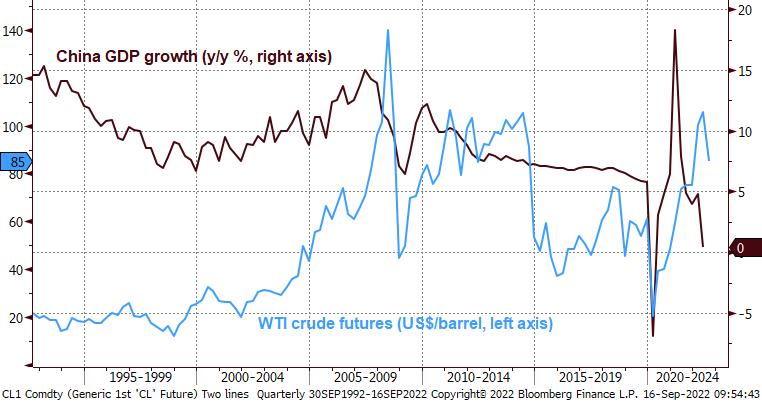

Crude prices were also impacted by news that China plans on ramping up its own oil exports. That headline might seem surprising, given that China ranks way down the list in terms of crude exports. Instead, it is that they are exporting oil at all that is rocking the market since this means consumption is way down. No surprise given how the country has been working with an incomplete covid policy for months and it is showing up in domestic demand. China actually plays a bigger role in terms of debate over the longer-term outlook for crude.

As the above chart shows, crude oil demand began to really take off two decades ago, when Chinese GDP growth accelerated from around 6% to a peak of 15% in 2007. True, China had seen larger growth numbers previously, but these were coming off relatively smaller gross output levels. In 1992, China’s economy was about US$425 billion. By 2007, it had grown to about US$3.5 trillion. If you do the math, a 15% growth rate in domestic output in 1992 was worth about US$16 billion, but it came out to US$525 billion in 2007. The problem is that China’s economy has all but stalled this year, despite attempts by Beijing to re-stimulate activity. The housing market is a mess and businesses, and consumers can’t get any traction with lockdown after lockdown. Even the economy recovers, it is doubtful China returns to its glory growth days. Keep in mind also that China also wants to clean up its energy impact.

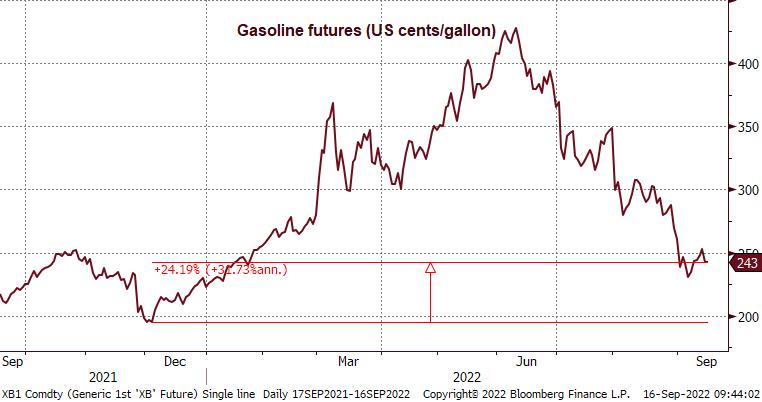

As much as oil prices have tumbled, taking other fuel prices down with it, we are not exactly trading at cheap levels. If we look back to the lows for WTI and gasoline futures back last December, we are up about 30% and 24%, respectively. That appreciation has weighed on business margins and household budgets, contributing to the slowdown that has already been reinforced by rising interest rates. The declines have been welcome, however, there is still a lot upward price pressure built into services and this is going to cause a further retrenchment in overall spending. If we could make an assumption that there would be no further increases in central bank rates, then economic demand could stabilize, and this would fuel (pardon the pun) some upside for crude prices.

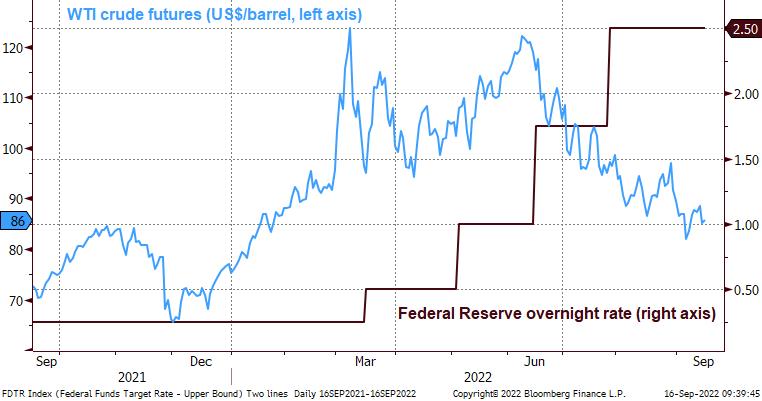

Unfortunately, the US CPI numbers this week basically sealed the deal on another 0.75% rate hike by the Federal Reserve next week. Moreover, Fed officials appear wedded to further tightening in the fourth quarter. Whether further rate hikes take place and how large they will be remains a mystery for now. What we do know is that monetary policy works with lags. The Fed raised rates a total of 1.5% from March to June, even as crude prices were climbing. The impact of that tightening started to show up in June and created the catalyst for the correction in oil demand. The more recent 0.75% hike in July only reinforced the demand destruction and we are days away from the next move.

Until rate cycle concludes, it makes sense that crude prices can continue their decline – potentially through $70 and possibly a retest of last December’s low of $65. That would put us close to the 5-year moving average, which actually bottomed just above $50 before the pandemic and has held above despite the plunge back in the Spring of 2020. Unless we see a major and prolonged recession, we might just be approaching the bottom for this cycle.

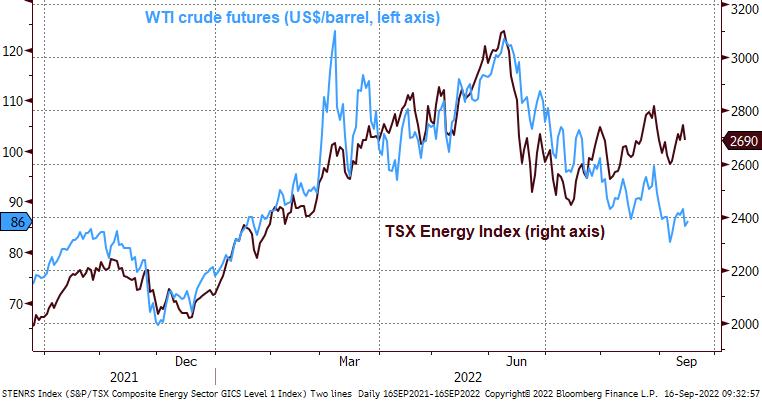

That would be good news for the energy patch, although the TSX energy sub-index has actually performed well over the last month and a half, despite the extended slide in crude. The group is off about 2.4% since the end of July while WTI futures are down 12.9%. If we did get an additional slip towards $70 in the wake of the next Fed hike, I would expect the group to push down to possibly re-test the mid-July lows, but that could represent an opportunity. Dividend yield for the sector is back in the 4.4-4.6% region – not quite back to the highs seen at the start of the year, but attractive, nonetheless.

Have a great weekend everyone

Andrew Pyle

CIBC Private Wealth consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc. “CIBC Private Wealth” is a registered trademark of CIBC, used under license. “Wood Gundy” is a registered trademark of CIBC World Markets Inc. This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2022.CIBC Wood Gundy, a division of CIBC World Markets Inc.

These are the personal opinions of Andrew Pyle and the Pyle Group and may not necessarily reflect those of CIBC World Markets Inc.

Related posts

Andrew Pyle

August 19, 2022

Value in banks?

Canadian bank earnings will start to flow out next week and, after a decent recovery in recent weeks, the question for investors is whether there is still more upside.

Read moreAndrew Pyle

October 14, 2022

Is this too early for tax-loss harvesting?

We typically look at tax-loss strategies towards year-end, but with market weakness this year, some investors may not be looking at significant realized gains. Even so, the continued correction might ...

Read more