Andrew Pyle

October 04, 2022

Psychology, not market, volatility

Last month, I commented on how observed market volatility had not yet reached levels that one would associate with panic. Yes, the CBOE VIX index pushed above 30, but this is below where we got in March, May and June during those sell-off episodes. Last week saw the same story play out where investors got extremely anxious over the thought of continued aggressive tightening by central banks and how this would likely trigger a major economic recession. What a difference a couple of days make.

The weekend was spent digesting the odds over whether interest rates were closer to a top than the bottom, which was followed by an about face by the new UK prime minister and chancellor of the exchequer on their unfunded lowering of the top tax rate. Equities bounced and this pendulum shift in sentiment was fueled by signs that the US economy was indeed slowing. Surely, the Fed would have to reconsider massive rate hikes at its November and December meetings?

Again, we have played this story out before where bad economic news is good news for stocks because it offers hope that rates will not rise appreciably from here and kill off the economy. The gains from Friday are impressive to say the least, with the major North American indices up close to 5% at the time of writing. The question is whether investors were irrationally bearish last month or whether they are irrationally bullish now? I would argue that both are correct and that we are a critical period of data watching. Nerves have been frayed by the end of summer correction, but now there is a sprinkling of optimism that the tightening cycle is coming to a close. The appropriate advice today is to not get emotionally entangled with this volatility in sentiment and focus on both fundamentals and technicals.

We know for a fact that there was a massive inflow of cash into money market funds over the course of the summer, as interest rates moved higher. That works against stocks at the moment, but it provides fuel for a rebound when the environment is right. We did anticipate that economic numbers would start to look bleak, but there is key report coming out this Friday and that is the US jobs data. A firm number could unravel a lot of what we have seen these two days.

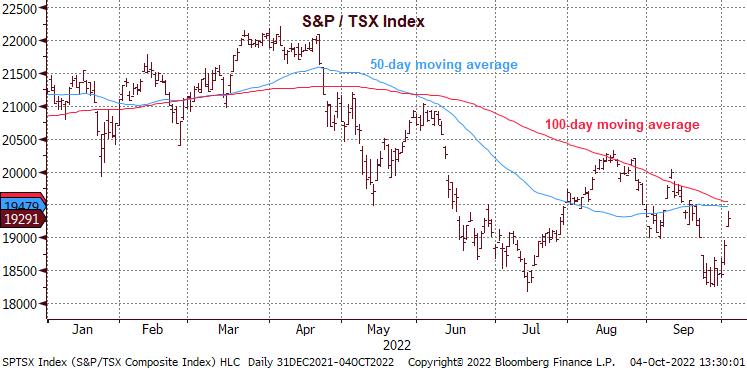

For the TSX, we are also approaching a key area around 19,500 – where both the 50-day and 100-day moving averages are converging. To snap out of the six-month pattern of lower highs, we will need to see this level breached. If not, and we get a reversal, then it is equally important the TSX finds support in the 18,150 to 18,250 area (18,170 was the intraday low on July 11th). Be prepared for investor psychology to swing around a lot in the coming days and weeks, until the interest rate path is clear.

On behalf of the Pyle Group, have a wonderful day.

Andrew Pyle

CIBC Private Wealth consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc. “CIBC Private Wealth” is a registered trademark of CIBC, used under license. “Wood Gundy” is a registered trademark of CIBC World Markets Inc. This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2022.CIBC Wood Gundy, a division of CIBC World Markets Inc.

These are the personal opinions of Andrew Pyle and may not necessarily reflect those of CIBC World Markets Inc.

Related posts

Andrew Pyle

June 17, 2022

Market volatility underscores the need for advice

This week's events have led to confusion among investors and apparently policy-makers too. Even though the economy is cooling off, markets are still fixated on mega rate hikes. This has led to selling...

Read moreAndrew Pyle

November 18, 2022

The income competition between stocks and bonds heats up

With bond yields up appreciably over the past year and most signs pointing to a recession in 2023, dividend paying stocks are in a less attractive position relative to bonds.

Read more