Bram Houghton

April 10, 2023

Economy Commentary

Bi-Weekly Market Update – April 6, 2023

Wicks Houghton group BI-Weekly Market Update

The March S&P Global Canada Manufacturing Purchasing Managers' Index (PMI) contracted to 48.6 in March 2023 after two months of expansion (Expansion is any reading > 50). Broader macroeconomic uncertainty and rising prices impacted heavily on consumer demand.

Canadian exports and imports decreased in February. The trade surplus also narrowed for February, with exports decreasing by more than imports for the month.

The Canadian economy added 35,000 jobs in March, more than the market expectations for an increase of 12,000. Canadian average weekly earnings of non-farm payroll employees rose 2.9%, in line with expectations.

The U.S. manufacturing sector contracted further in March, with the ISM Manufacturing Purchasing Managers' Index (PMI) fell to a 21-month low of 46.3 from 47.7 in February, well below consensus forecasts for a more modest drop to 47.5.

Growth in business activity in the services sector in the U.S. slowed by more than expected, with the ISM non-manufacturing sector index for March dipping to 51.2, down from a previous reading of 55.1 in February and 55.2 in January.

U.S. initial jobless claims came in higher than expected, rising by 18,000 to 228,000 vs. 200,000 expected. Job cuts have also increased by nearly fivefold so far this year from a year ago. U.S. private employers in March hired 145,000, well below the estimate of 210,000. This suggests the labor market is showing signs of cooling.

U.S. fourth quarter Gross domestic product (GDP) was revised to an annual growth rate of 2.6%, slightly less than initial estimates of a 2.7% rise. U.S. consumer spending rose 1%, below the 1.4% forecast.

February U.S. inflation measured by Personal Consumption Expenditures (PCE) index rose 0.3% vs. the expected 0.4% from the previous month. On a yearly basis, the PCE index rose to 4.6%, the least in 15 months. It was also below market expectations of 4.7%.

Euro Zone Inflation eased to 6.9 percent in March 2023, its lowest level since February 2022. Spain’s annual inflation rate fell to 3.3% in March, with electricity and fuel prices falling. German states also reported softer inflation dropping to 6.9% in March from 8.5% a month ago.

German business outlook unexpectedly rises to highest in year while U.K. outlook is positive as recession and cost of living fears recede. German industrial orders rose more than expected in February, driven by a strong growth in the vehicle construction sector.

China's PMIs jumped to 58.2 in March from 56.3 in February, marking the best level since 2011. Profits at industrial firms in China declined 22.9% year over year in January to February, weighed by lackluster demand and stubbornly high costs.

West Texas Intermediate crude oil prices rose on expected rising Chinese crude demand and lower Russian production. OPEC+ also announced a surprise production cut of 1.16 million barrels per day which will start in May, led by an output reduction from Saudi Arabia. U.S. crude stockpiles also fell sharply for a second week in a row, storage fell by 3.739 million barrels during the week ended March.

Bloomberg Market Updates - https://www.bnnbloomberg.ca/markets

Schwab Market Updates Podcasts - https://www.schwab.com/resource-center/insights/section/schwab-market-update

| Market Data | S&P/TSX | S&P 500 | DOW | NASDAQ | STOXX EU | WTI | GOLD |

| This Week | +0.5% | -0.4% | +0.6% | -1.1% | +1.0% | +6.3% | +1.9% |

| Last Week | +3.1% | +3.5% | +3.2% | +3.4% | +3.6% | +9.2% | FLAT |

2023 FEDERAL BUDGET – Top takeaways as summarized by Jamie Golombek, Managing Director, Tax and Estate Planning, CIBC Private Wealth

What’s not in it

Good news to many that there was no sign of increases in tax rates or the capital gains inclusion rate, and no changes affecting corporate class structures or return of capital strategies.

Grocery rebate

The budget proposed eligible individuals to receive twice the GST rebate for January 2023, which is to be paid ASAP after legislation is passed. maximum official amount will be $153 per adult or $81 per child, and another $81 for a single supplement.

Alternative Minimum Tax (AMT) & General Anti-Avoidance Rule (GAAR)

From 2024, the government, being concerned that high income individuals are paying relatively little in personal income tax as a share of their income has completely rehauled the alternative minimum tax known as the AMT. The GAAR will be amended to help address the various interpretative that could cause GAAR to not be applied as intended.

Registered Education Savings Plan

$8,000 of Educational Assistance Payments (EAPs) allowed in the first 13 consecutive weeks of enrollment and divorced/separated couples can open an RESP as joint subscribers.

Corporate Tax Changes

The government is just making a couple of changes there to make sure that people don't take advantage of that rule inappropriately, if there hasn't been a bona fide sale to a family member. Legislation also introduced to facilitate employee ownership trusts

Global Insights

Portfolio Manager’s comments from Fidelity’s recent Fund Manager’s Conference

Dan Dupont, Fidelity Canadian Large Cap Fund, Fidelity Global Value Long Short

Outlook & Positioning

- The yield curve has been inverted 8 times in the last 50 years, and was followed by a recession all 8 times. It’s a powerful signal. But it usually takes 12-18 months for problems to arise. I think we’ll continue to see problems from here.

- I’m positioned fairly defensively, even more so than usual. I can change this positioning quickly if needed; in 2020 I did so within 2 weeks.

Thoughts on Real Estate

- Can these prices be sustained due to supply/demand? Immigration has become pro-cyclical. If we have less immigrants would that put pressure on house prices?

- Rent should be 0.5% of the house value. But that’s not the case right now. Maybe rents will keep going which would be tough, or maybe housing corrects.

Mark Schmehl, Fidelity Global Innovators Class, Fidelity Canadian Growth Company, Fidelity Special Situations Fund

Outlook

- I don’t think this recession will be as bad as ‘08. I think it will be more similar to the 90s recession, more textbook. I don’t think we’ll hit a new low. We may retest the October low. I think the recession will be short.

- It’s too soon to be really bullish, but I am continuing to try to find the bottom. It’s more of a slow and steady shift. I think it will be at some point later this year or early next year. Overall I see the market being in a much better place in 12-18 months and I want to get ahead of it.

- I think different sectors will bottom at different times. Currently tech has gotten pulverized, and it will spill into other parts of the economy because Tech is one of the largest sectors in the US.

MacroMemo - March 28 – April 11, 2023 by Eric Lascelles Link to Article

Efforts to halt additional bank runs

The US government has created a Bank Term Funding Program at the Federal Reserve to prevent further bank runs. This facility allows US banks to swap their bond holdings for a cash loan for up to a year, with the bonds swapped at face value rather than market value. Over $300 billion has been tapped in the past two weeks, reflecting its success, but borrowing is expensive at 4.7% interest. The facility aims to help viable banks survive a near-term bank run, and in theory should be enough to halt further runs, although there is still some stress in the market.

How is this different than the global financial crisis?

The global financial crisis of 2007-2009 was much worse than recent banking sector stress because banks were less well capitalized and regulated. The average bank today has more capital, but during the crisis, there were severe housing market problems, lax lending standards, and the creation of exotic securitized assets that led to greater bank losses. The disintermediation of toxic assets and a lack of transparency made it difficult to anticipate problems. In contrast, modern-day problems are those of a classic bank run at a few vulnerable financial institutions that the US government has credibly addressed through policy solutions.

Economic Developments

The economic news from the developed world has been holding up surprisingly well, with no recession in sight yet. In February, the North American employment numbers were robust, with the US adding 311,000 new jobs and jobless claims staying low. Similarly, Canada added 22,000 new workers, which was lower than the previous month but entirely full-time. Additionally, February saw a mixed bag of data in the US, with retail sales falling by 0.4%, industrial production staying flat, and core capital goods orders going up by 0.2%. While real-time economic data was softer, with Bank of America's real-time card spending measure claiming no increase in consumer spending compared to the previous year, stronger retail sales and higher personal consumption over the same period contradict this claim.

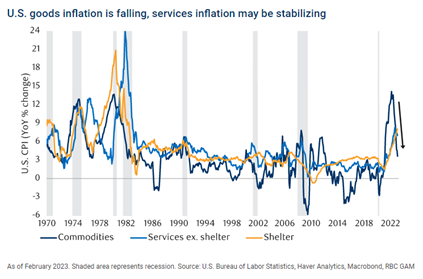

Stubborn inflation

Inflation in the US continues to decrease from its peak, but the rate of improvement has slowed down. In February, the US Consumer Price Index (CPI) fell from 6.4% to 6.0%, and core inflation declined from 5.6% YoY to 5.5%. However, headline and core prices rose by 0.4% and 0.5% respectively versus the prior month. Goods inflation is now cooperating nicely, but service-sector inflation remains too high. Inflation has been particularly consequential in four big price categories: motor fuel, transportation ex motor fuel, housing, and food and beverages. The motor fuel driver has completely reversed over the past several months, and the transportation component is nicely decelerating as used car prices fall. The housing component of inflation is not yet cooperating, but home prices are falling and rent increases are slowing. In Canada, inflation in February fell from 5.9% YoY to 5.2%, but the monthly change was still +0.4% for the month. Goods inflation is cooperating while service inflation is much more resistant to decline.

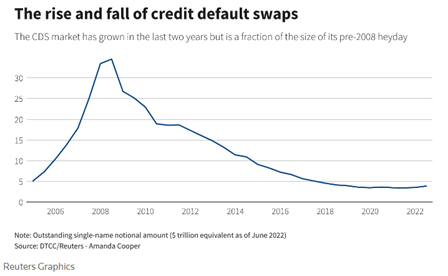

Explainer: What are credit default swaps and why are they causing trouble for Europe's banks? Reuters

Turbulence in Europe's banks following the implosion of 167-year-old Credit Suisse and runs on regional banks in the U.S. has focused attention on the role played by credit default swaps in all the turmoil.

Bond investors hope to receive interest on their bonds and their money back when the bond matures. But they have no guarantee either of these things will happen and so have to bear the risk of holding that debt. CDS help to mitigate the risk by providing a form of insurance against a company defaulting on their bond obligations.

When you read the content we share and it causes you to think of others in your life who would benefit from seeing it, please don’t hesitate to share it with them.

CIBC Private Wealth Management consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc.

"CIBC Private Wealth Management" is a registered trademark of CIBC, used under license. "Wood Gundy" is a registered trademark of CIBC World Markets Inc.

If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2022.

Related posts

Bram Houghton

October 14, 2025

Market Update - September 8th - October 10th, 2025

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read moreBram Houghton

September 10, 2025

Market Update - August 2025 Edition

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read more