Bram Houghton

April 27, 2023

Economy Commentary

Weekly Market Update – April 21, 2023

Wicks Houghton group BI-Weekly Market Update

The Bank of Canada (BoC) held the target for its overnight rate at 4.5% as expected. The BoC stated it will continue to monitor economic data for future decisions on the policy rate.

Inflation in Canada continued to decline in March, with the annual rate falling to 4.3% from 5.2% in the prior month. Lower energy prices were the main reason for the deceleration, although higher mortgage interest costs provided some upward pressure.

Canadian Retail sales decreased though less than expected in February, on lower sales at gasoline stations and general merchandise retailers. Sales decreased in four of nine subsectors, representing 48% of retail trade.

Canadian home sales rose 1.4% in March 2023 from February 2023. This is the second straight month of higher sales, but sales were down 34.4% on an annual basis.

March housing starts in Canada slipped by 11% to 214,000 units, below the expected and well below February starts. Groundbreaking decreased on multiple-unit and single-family detached urban homes as homebuilding appears to be slowing under the weight of higher interest rates.

The U.S. March CPI showed a rise of 0.1% vs. expectations of a 0.2% rise month over month. The 12-month increase in CPI slowed to 5% vs. the 5.2% expected, down from 6% in the prior month. The annual core CPI rate ticked up to 5.6% from a 14-month low of 5.5% in February.

U.S. retail sales fell more than expected in March, dropping by -1% vs. the -0.4% expected. This is a sign that cost pressures and rising interest rates are weighing on consumer spending. U.S. March core retail sales slipped -0.8% vs. the -0.3% forecast.

U.S. initial jobless claims rose over the last two weeks, increasing by 16,000 to 245,000 above forecast for both weeks. This is the highest level in more than a year but remains at relatively low levels. This is a sign the labor market has cooled slightly as higher interest rates dampen U.S. growth.

U.K. March CPI came in at 10.1% vs. 9.8% expected, down from 10.4% in February. The U.K. economy also flatlined in February but revised January figures show gross domestic product back at pre-pandemic levels. Retail sales fell more than expected by 0.9% in March from February.

The annual inflation rate in the Euro Area was 6.9% in line with expectations, its lowest level since February 2022.

The European Union agreed a 43-billion-euro plan for its semiconductor industry to catch up with the United States and Asia and start a green industrial revolution.

Oil prices were down over the two weeks as slowing global demand and interest rate hike expectations weighed on OPEC producer supply cuts.

China’s new home prices rose at the fastest pace since Jun-2021 in March, signaling relief for the property sector. China is starting to target foreign companies after US-led tech blockade. G7 diplomats and officials are to discuss China's military threats to Taiwan.

China’s gross domestic product rose by 4.5% in the first quarter of 2023, beating estimates of 4%. The International Monetary Fund says China will be top contributor to global growth over the next five years, representing 22.6% of the total increase.

Bloomberg Market Updates - https://www.bnnbloomberg.ca/markets

Schwab Market Updates Podcasts - https://www.schwab.com/resource-center/insights/section/schwab-market-update

| Market Data | S&P/TSX | S&P 500 | DOW | NASDAQ | STOXX EU | WTI | GOLD |

| This Week | +0.5% | FLAT | -0.2% | -0.4% | +0.8% | -5.5% | -1.0% |

| Last Week | +1.9% | +0.8% | +1.2% | +0.2% | +1.6% | +2.3% | -0.5% |

CIBC Economics Quick Take: Bank of Canada rate decision by Avery Shenfeld

The Bank of Canada has left its overnight rate unchanged at 4.5% and warned that it may have to hike again if the economy fails to slow down to quell price and wage pressures. Despite the upside surprise in Q1 growth, the Bank believes that a desired slowdown is still expected due to international influences and the lagged impact of prior rate hikes on Canadian households and business investment. The Bank's growth outlook for 2023 has been raised, while the inflation outlook has remained unchanged. The Bank remains on hold, but not in sync with market expectations for rate cuts this year, as it is not calling for a recession.

ECONOMIC FLASH! Canadian CPI (Mar): Descending steeply, but still too high by Andrew Grantham Link to Article

Inflation in Canada continued to decline in March, with the annual rate falling to 4.3% from 5.2% in the prior month, and the Q1 average slightly below the Bank of Canada's MPR forecast. Lower energy prices were the main reason for the deceleration, although higher mortgage interest costs provided some upward pressure. While food price inflation slowed, prices continued to rise on average on a month-to-month basis, which is in slight contrast to the US figures. Core measures of inflation also showed slower trends than in mid-2022, but remains above the Bank of Canada's 2% inflation target. Policymakers will likely maintain a hawkish tone for now, with interest rate cuts not expected until next year.

CIBC Economics Forecast: Inflation continues to ease and will do so further as some of the largest increases from 2022 drop off the yearly calculation, likely stalling in the 2.5- 3.0% range. That should be low enough to prevent further rate hikes, but not yet to a level at which policymakers will feel confident about easing interest rates.

How bad is the good news? by Avery Shenfeld Link to Article

The Canadian economy has shown strong growth in the first quarter of 2023, with an expected 3% GDP increase, above the Bank of Canada's projection of 0.5%. However, this growth is not necessarily bad news for inflation, as it may be due to increased workers and improved supply chains which could help non-inflationary growth. Nevertheless, weak productivity growth may be a challenge, and growth may slow in the future. The Bank of Canada may not join the market's thinking about rate cuts as it requires bad news in the form of higher unemployment and output drop for a quarter or two to do so.

Global Insights

MacroMemo - April 12 -24, 2023 by Eric Lascelles Link to Article

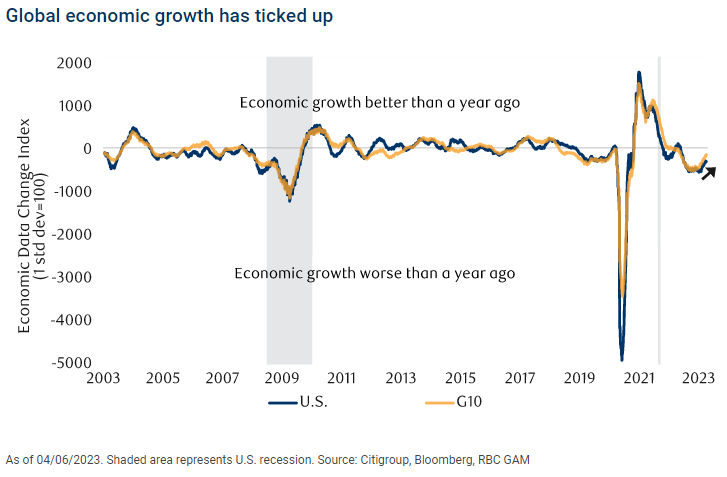

Economic resilience

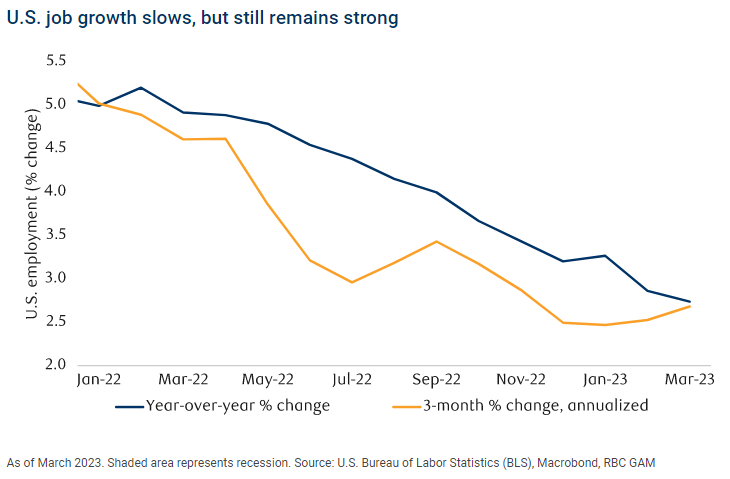

The economic data across the G10 countries has improved in the past few quarters, but it is not yet indicating strong growth. The global manufacturing PMI has moderately increased, but the level is low. However, economic data has been positive, exceeding expectations over the period. Despite job creation being slower in the US than last year or two, 236,000 jobs were added in March leading to a decrease in unemployment. In Canada, 35,000 new jobs were added in March, maintaining a low unemployment rate of 5.0%. However, some exceptions remain, such as the U.S. Institute for Supply Management Manufacturing Index which continues to fall and is now near the historical recession threshold.

Waiting on inflation

There is evidence suggesting that inflation may have decreased in March, but there are still issues with core services and shelter costs that need to be addressed. The consensus outlook is for inflation to be lower in 2023 and 2024, but it will still remain moderately above 2.0%. The international outlook is slightly more promising, with fewer countries experiencing rising inflation forecasts.

Tight economy

The best predictor of core services ex shelter inflation is the tightness of the labour market and economy. There are differing opinions on the size of the U.S. output gap, with estimates ranging from 1.0 to 1.7 percentage points beyond its sustainable capacity. The average estimate is that the economy is moderately overheating and may need to cool down to fully normalize inflation. It is evident that, based on the lingering resilience of the economy, that a recession may be needed to help achieve the inflation objective.

How to Lose Reserve Currency Status by Brian S. Wesbury Link to Article

The US and the dollar could potentially face the same fate as other societies and currencies throughout history, but it is unlikely to happen anytime soon.

The US became a dominant economic power due to the rule of law, private property rights, democracy, and a strong culture that fostered entrepreneurship and progress. However, the US is currently on a path of excessive government spending and monetary policy that could lead to the decline of the dollar. The Federal Reserve's experimental "abundant reserve" policy has flooded the financial system with liquidity, and government spending now controls 45% of US output. To prevent the decline of the dollar, the US needs to limit government spending, keep tax rates low, and return to a "scarce reserve" monetary policy.

While countries like China, Saudi Arabia, and Russia may have resources, they lack the freedom and policies that made America strong. It is unlikely that any of these countries will replace the dollar, but bad policies could lead to the decline of the currency in the future.

Notable News

Poland agreed on Tuesday to lift a ban on the transit of Ukrainian grain and food products, but Ukraine said a wartime deal allowing it to safely ship grain from Black Sea ports was still under threat.

Failure to resume exports into eastern European countries or secure an extension of the Black Sea grain deal would trap large amounts of grain in Ukraine, hitting its exports and causing further economic problems for Kyiv as it battles Russian troops.

The artificial intelligence behind ChatGPT, the homework-drafting chatbot that some schools have banned, is coming to more students via the company Chegg Inc.

The U.S. educational software maker has combined its corpus of quiz answers with the chatbot’s AI model known as GPT-4 to create CheggMate, a study aide tailored to students, CEO Dan Rosensweig told Reuters last week.

When you read the content we share and it causes you to think of others in your life who would benefit from seeing it, please don’t hesitate to share it with them.

CIBC Private Wealth Management consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc.

"CIBC Private Wealth Management" is a registered trademark of CIBC, used under license. "Wood Gundy" is a registered trademark of CIBC World Markets Inc.

If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2022.

Related posts

Bram Houghton

October 14, 2025

Market Update - September 8th - October 10th, 2025

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read moreBram Houghton

September 10, 2025

Market Update - August 2025 Edition

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read more