Bram Houghton

May 08, 2023

Economy Commentary

Market Update - May 5th, 2023

Wicks Houghton group BI-Weekly Market Update

In a nutshell: Economies in North America continue to hang on in the face of tightening economic conditions. While we had a strong two weeks for Corporate Earnings, particularly in the US and the labour market remains relatively resilient, GDP numbers were weak while the labour markets and general consumer began to show signs of fading as well, which are a couple of the primary indicators we are watching closely at this stage of the cycle.

Canada’s real gross domestic product edged up 0.1% vs. the expected 0.2% in February, following a 0.6% increase in January. Both service-producing industries and goods-producing industries edged up 0.1%.

The Canadian labour market remained strong in April, with employment rising more than expected, and wage inflation failing to decelerate. The gain in jobs during April was double consensus, although the quality wasn't quite as good as in prior months with all the gains being part-time work.

The S&P Canada Manufacturing PMI rose to 50.2 in April 2023, indicating a marginal expansion in the manufacturing sector after posting a near three-year low of 48.6 (contraction) the previous month. Output and employment both increased, but new orders fell modestly indicating firms were hesitant in their spending decisions due to higher prices and the uncertain direction of the economy.

Canada’s March New Housing Price Index was unchanged for the month. The index has been down in five of the last seven months. The Index increased by 0.2% yearly which is the lowest since January 2020.

Canada's exports though imports decreased more in March, causing a surprise trade surplus. The U.S. trade deficit narrowed in March versus forecasts.

U.S. GDP grew at slower than expected pace of 1.1% annual pace in first quarter, below forecasts of 2%. An acceleration in consumer spending was offset by businesses cutting back on inventory investment in anticipation of weaker demand this year amid higher borrowing costs. The GDP index report showed stronger inflation with prices increasing 4%, compared with an estimate of 3.7%.

After regulators took possession of First Republic Bank (FRC) on Monday, JPMorgan has agreed to purchase bank’s deposits and a substantial majority of the Bank’s assets. The seizure of First Republic resulted in the biggest bank failure since the 2008 financial crisis, when Washington Mutual collapsed.

U.S. job openings decreased and were below expectations in March. This is the lowest level since April 2021, a sign the labor market is cooling off. Despite this, initial jobless claims fell surprising market expectations, as the labor market remains tight.

The US labor market heated up in April, as hiring accelerated well above consensus although there was a downward revision to the prior two months which erased the upside surprise. Business services, health/social assistance, and leisure and hospitality led the job gains, while employment in goods-producing sectors rebounded following a drop in March.

United States ISM Services PMI increased to 51.9 in April from 51.2 in March. This is slightly better than the market consensus. It marks a fourth consecutive month of growth in the services sector, prompted by an accelerated increase in new orders.

The House of Representatives have narrowly passed a debt ceiling bill yesterday. House Republicans approved a bill aimed at capping government spending for a one-year increase of the country’s debt limit.

Oil prices were down over the two weeks as concerns over weaker Chinese manufacturing data and the U.S. Federal Reserve potentially raising interest rates outweighed OPEC+ supply cuts taking effect later this month.

Gold prices continued to strengthen over the two weeks as the US banking challenges saw investors turn to safe haven.

Bloomberg Market Updates - https://www.bnnbloomberg.ca/markets

Schwab Market Updates Podcasts - https://www.schwab.com/resource-center/insights/section/schwab-market-update

| Market Data | S&P/TSX | S&P 500 | DOW | NASDAQ | STOXX EU | WTI | GOLD |

| This Week | -0.5% | -0.8% | -1.3% | FLAT | -0.4% | -7.1% | +1.3% |

| Last Week | -0.3% | +0.8% | +0.9% | +1.3% | +0.8% | -1.4% | +0.5% |

Quick Take: US Fed rate announcement by Avery Shenfeld

As widely expected, the Fed opted to hike a further quarter point, but also avoided saying that they had reached a judgement that further hikes might be required. That wording was replaced by language saying that they would now monitor incoming information to decide whether more rate hikes are in fact needed, which suggests that they could be on hold for a while, as there will be need for some elapsed time before they would be able to make such a judgement, if the data isn’t overwhelmingly leaning towards stronger than expected growth and inflation. The change reflects new uncertainties over the banking system, which they describe as “sound”, while admitting that “tighter credit conditions”, which presumably would include both higher rates and recent banking developments, will weigh on growth and inflation, but to an uncertain degree. This is a hawkish pause, as the committee says it will be looking for signals on the need for additional firming, rather than a balanced statement that would have referenced potential moves in either direction. Similarly, they say they are “highly attentive” to inflation risks, with no similar statement on recession risks. But if, as we expect, Q2 sees little or no growth, and inflation signals continue to moderate, the May hike should prove to be the last for this cycle, with the first easing not likely until 2024, as we’ll also need time for inflation pressures to sufficiently abate.

Global Insights

MacroMemo - April 25 - May 15, 2023 by Eric Lascelles Link to Article

Banking stress

Following the failure of two US regional banks, there remains some stress in the banking system, with deposits fleeing and demand for emergency loans declining but still high. Concerns about banks' ability to repay their debt have eased but many banks have lost significant amounts of money on their bond holdings as interest rates rose.

This has left banks less liquid and more capital-constrained, leading to tighter lending standards and a decline in US commercial industrial loans. The decline may not yet be over, with a rising number of small businesses now expecting tighter credit ahead. These factors will contribute to economic damage, particularly for bank-reliant mid-sized and smaller businesses, and smaller US banks will face increased regulation and reduced profitability. This will further reduce their ability to lend, impacting the commercial real estate sector and smaller business clients. At the most negative end of the spectrum, this situation could develop into a crisis like the US savings and loan crisis of the 1980s and 1990s.

Labour supply revival

The supply of labour in the US fell dramatically during the pandemic due to illness, fear of infection, childcare issues, government transfers and high household wealth. Although hiring surged and unemployment rates fell as the pandemic receded, the labour force participation rate remained well below the pre-pandemic level as many workers were reluctant to return. However, missing workers began to return to the labour force in 2022 and 2023, reducing the gap only marginally when demographics are considered. The recent leap in the labour force participation rate has prevented the job market from overheating, with the supply of labour unexpectedly keeping pace with demand due to factors such as falling household savings, retirement account valuations and home prices, and the availability of jobs and strong wage growth. As a result, the US economy is not significantly tighter than a year ago, which has implications for central bank policy.

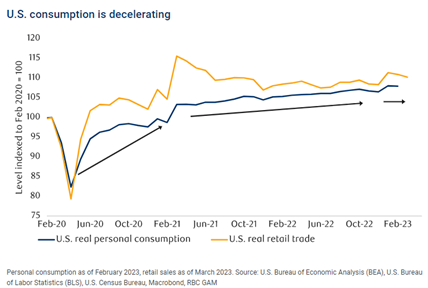

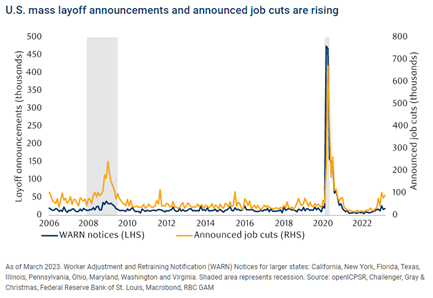

Softening job market

Although hiring has been strong, there are signs of weakness at the edges of the US labour market. The share of temporary employment is falling, as are the quits rate and job openings, with alternative measures suggesting a steeper decline than official data. In addition, US jobless claims are increasing, reaching a 26% increase relative to early 2023. Two measures of mass layoffs are also starting to increase, which traditionally indicates impending job losses and a recession.

If you don’t know where you’re going (The Week Ahead) by Avery Shenfeld Link to Article

The US Federal Reserve knows where it wants to go - a 2% inflation rate - but is uncertain about the path to get there due to concerns around regional banks and a retrenchment from bloated liquidity seen during the pandemic. Final demand was healthy in Q1, but spurred by one-off tax relief and slowing job gains. The economy showed less momentum at the end of the quarter, and most interest-sensitive sectors are in decline. The Fed is willing to raise rates by another quarter point, but there is a hole in its ability to assess the impact of banking system failures or regional bank funding squeezes. The Fed needs time to gain further insight into the drag from regional bank developments, and our call is for May's move to be the final hike for this cycle, with the FOMC waiting until 2024 to start cutting rates.

Notable News

Credit Suisse said on Monday that 61 billion Swiss francs ($68 billion) in assets left the bank in the first quarter and that outflows were continuing, underscoring the challenge faced by UBS Group (UBSG.S) in rescuing its rival.

"These outflows have moderated but have not yet reversed as of April 24, 2023," Credit Suisse said, adding that most of the money leaving the bank was from its wealth management division and occurred across all regions. The net asset outflow followed 110.5 billion francs pulled by clients from the bank in the fourth quarter.

U.S. Treasury Secretary Janet Yellen said in January the government could pay its bills only through early June without increasing the limit, which the government hit in January.

Some analysts had forecast the government would exhaust its cash and borrowing capacity - the so-called "X Date" - sometime in the third or fourth quarter, but weaker-than-expected tax receipts for the April filing season could pull that deadline forward.

Wicks Houghton Group – It is highly unlikely that no agreement is reached (per previous cases in 2011, 2013, 2021) however, this will consume US government resources and headlines for some time.

When you read the content we share and it causes you to think of others in your life who would benefit from seeing it, please don’t hesitate to share it with them.

Related posts

Bram Houghton

October 14, 2025

Market Update - September 8th - October 10th, 2025

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read moreBram Houghton

September 10, 2025

Market Update - August 2025 Edition

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read more