Bram Houghton

August 14, 2023

Economy Commentary

Bi-Weekly Market Update - August 11th, 2023

Wicks Houghton group BI-Weekly Market Update

IN A NUTSHELL: Plenty of news over the last two weeks with economic signals continuing to be mixed. Most significantly, the US Treasury downgrade created headlines that the US government can’t ignore about their expanding fiscal deficit. US CPI trended positively and conditions also eased in the Eurozone. Labour markets cooled in North America while Canada saw trade weaken to levels not seen since 2020.

Canada's economy grew 0.3% in May and likely contracted in June, pointing toward a slowdown that could bring an end to the central bank's monetary tightening campaign that has pushed interest rates to a 22-year high. The expansion in May was in line with expectations and the report suggests a 1% annualized GDP rate, which is lower than the BoC's forecast of a 1.5% for Q2.

Canada’s July employment report unexpectedly shed jobs by 6,400 against an expectation of 25,000 job growth. Canada’s July unemployment rate also edged up slightly to 5.5% from 5.4% in June.

Canada's trade deficit widened by 40% or C$1 Billion in June, the largest in nearly 3 years. Exports decreased 2.2%, while imports declined 0.5%.

The US economy added fewer jobs than expected in July, while the number of positions added in the previous two months was revised lower, in a sign that a long-standing string of aggressive interest rate hikes by the Federal Reserve may be weighing on the labor market. Growth in average hourly earnings was unchanged on a monthly basis and, annually, wages increased by 4.4%, outpacing projections of 4.2% and more than double the Fed's target of 2%.

The US consumer price index rose to 3.2% in July though below expectations of 3.3%, and from 3% in June. The annual core inflation rate decreased to 4.7% in July from 4.8% in June.

The US trade deficit narrowed sharply in June as businesses cut back on purchases of foreign-made capital goods, resulting in imports falling to the lowest level in more than 18 months. The trade deficit contracted 4.1% and data for May was revised to show the trade gap narrowing from previously reported.

Rating agency Fitch downgraded the US government's credit one level from AAA to AA+. This follows the cut by S&P in 2011, leaving Moody’s as the only major rating company keeping its top-tier grade for the US.

Americans borrowed more than ever on their credit cards in the last quarter, with balances surpassing $1 trillion for the first time even as overall household debt loads were largely unchanged. Credit card balances rose by $45 billion to $1.03 trillion in the second quarter, reflecting robust consumer spending as well as higher prices due to inflation, researchers said.

US labor costs increased less than expected in the second quarter as wage growth cooled, offering a boost to the Federal Reserve in the fight against inflation. The ECI is widely viewed by policymakers and economists as one of the better measures of labor market slack and a predictor of core inflation, because it adjusts for composition and job-quality changes.

The euro zone returned to growth in the second quarter of 2023 expanding by 0.3%, above expectations in the second quarter after narrowly avoiding a technical recession around the turn of the year.

Euro zone inflation fell further in July and most measures of growth also eased which was a comforting sign for the European Central Bank. Consumer prices grew by 5.3% this month versus 5.5% in June, extending a downwards trend that started in the fall.

British lenders approved more mortgages than expected in June and net unsecured lending to consumers shot up by the most in over five years, despite rising interest rates. Banks and building societies approved the most mortgages since October 2022 when the housing market faltered after Liz Truss' tax cut plans.

Chinese manufacturing activity contracted for a fourth straight month in July, faced with weak demand and laggard private spending. The official manufacturing purchasing managers’ index was 49.3 in July which was slightly higher than expectations of 49.2 and the prior month’s reading of 49.0.

WTI continued its steady trend upwards for the two weeks as strong US demand, Saudi and Russian output cuts and optimistic demand forecasts from the OPEC producer group and the International Energy Agency offset concerns about slow demand from China.

Bloomberg Market Updates - https://www.bnnbloomberg.ca/markets

Schwab Market Updates Podcasts - https://www.schwab.com/resource-center/insights/section/schwab-market-update

| Market Data | S&P/TSX | S&P 500 | DOW | NASDAQ | STOXX EU | WTI | GOLD |

| This Week | +0.8% | -0.3% | +0.6% | -2.0% | +0.8% | +0.3% | -1.5% |

| Last Week | -1.4% | -2.3% | -1.1% | +4.4% | -2.5% | +2.8% | +0.8% |

CIBC Economics Quick Take: Canadian employment (Jul) by Andrew Grantham

As is often the case, today's employment report brought mixed messages for the Bank of Canada, with the job count declining unexpectedly but wage growth accelerating much more than anticipated. The 6,400 decline in employment came against consensus expectations for a 25,000 increase.

By sector, the biggest drop was seen in construction. The decline in the job tally meant that, despite a slight dip in labour force participation, the unemployment rate rose to 5.5% (in line with the consensus). However, despite the softer job tally, wage growth spiked back up to 5.0%, which was much higher than the 4.1% consensus expectation. As a result, today's data is unlikely to convince the Bank of Canada that the labour market has loosened enough yet to sustainably achieve its 2% CPI target, despite the weaker headline jobs count.

Still living the high life? by Avery Shenfeld Link to Article

Over the past two-three years, many Canadians have been able to accumulate a larger pool of savings due to reduced spending on travel, movies, and restaurants. The Bank of Canada expressed concerns that this excess savings might dampen the response to higher interest rates, leading to a deeper decrease in incomes to curb spending. However, a closer look at the data suggests that the increase in liquid financial assets is not necessarily indicative of Canadians being "richer than they think", and reflects a larger share of total household financial assets, GICs and other high-interest rate vehicles being preferred over stocks and bonds.

It is also apparently that through the high inflation and interest rate environment that overall household net worth has declined, indicating that Canadians are not unusually flush with spending power. As a result, as interest rates rise and job growth slows, Canadian households may respond differently to financial pressures compared to the wealthy.

MacroMemo – August 1st – 21st by Eric Lascelles Link to Article

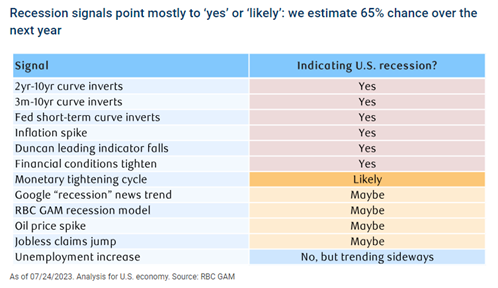

Business cycle signals recession?

According to the latest quarterly update on the US business cycle, there are interesting developments. The scorecard has shifted from indicating the "end of cycle" to "recession", but the interpretation is not straightforward. While some economic variables have continued to progress, a larger number have regressed, leading to a split distribution. The "recession" signal likely implies that a recession is on the horizon, rather than already underway.

However, it is also possible that the current state represents the worst point in the cycle without an economic contraction. The interpretation with the highest likelihood is that a recession is impending, although the mixed signals from the scorecard introduce some uncertainty.

Central banks near the finish line?

Many developed-world central banks, including the US Federal Reserve, may be nearing the end of their recent monetary tightening. The Federal Reserve recently delivered a 25 basis point rate increase, bringing the upper end of the fed funds rate target range to 5.50%. While there is still a possibility of another rate hike, financial markets believe the Federal Reserve is likely done for now.

The Bank of Canada and the European Central Bank have also taken data-dependent stances, while the Bank of England is an exception with expectations of three or more rate increases. The Bank of Japan, which recently experienced some inflation, has become more tolerant of higher inflation as a tool to revive long-term inflation expectations. Meanwhile, some emerging market economies have started cutting their policy rates, potentially signaling the beginning of an easing cycle.

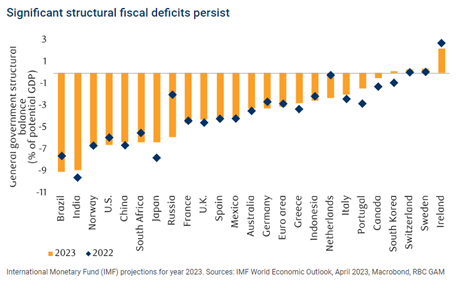

A fiscal thought

Governments are under more pressure than ever to spend on programs such as green initiatives and increased military capability, support aging populations and servicing debt. Despite the optimism of the easiest solution, growing the economy, weakening trade and technological uncertainty present unpredictable problems.

Tax hikes and spending cuts, meanwhile, are both highly unpopular so it is likely fiscal allowances will be made via interest rate repression and tolerating slightly higher inflation until fiscal austerity plans take hold. Fiscal austerity will ultimately be the predominant solution to driving down debt with a bit of extra help from long-term growth and interest rate repression.

Structural deficits persist across many countries according to the IMF, with many facing deficits that have expanded beyond that of 2022. US is one of those countries whose fiscal deficit has expanded in 2023.

Something to “Fitch” About Brian S. Wesbury Link to Article

Fitch Ratings recently downgraded US Treasury debt from AAA to AA+ due to massive deficits, fiscal deterioration, and erosion of governance. This follows a similar downgrade by Standard & Poor's in 2011.

The US Treasury has borrowed $1.1 trillion in just two months, as tax revenue falls and spending has increased significantly. The government's response to the COVID-19 pandemic, including lockdowns and economic relief, has led to increased borrowing and taxation, causing collapsing revenues. Emergency spending tends to become permanent, leading to higher deficits and a larger government that hinders economic growth. Entitlement programs for seniors, Social Security and Medicare will further contribute to the fiscal imbalance in the future.

Both parties are responsible for the current situation, and both need to be involved in finding a solution to what is absolutely clear: Cutting spending is necessary to address the budget fiasco before it becomes irreversible.

NOTABLE NEWS

This is a fantastic infographic on some of the less talked about ways greenhouse gases are created and how we can make a difference. I certainly learnt something from this!

The trashcan is a common place for disposing of old food, but climate scientists ask us to think twice before condemning our food to landfills where it breaks down and releases a significant portion of human-made greenhouse gases.

Over time, food is buried under other waste and decomposes in anaerobic conditions (without access to oxygen), creating a favorable environment for bacteria that produce methane, a greenhouse gas 28 times stronger than carbon dioxide over a 100-year period.

Niger's regional and Western partners have announced a series of sanctions against the country following last week's coup. Niger is the world's seventh-biggest producer of uranium, the radioactive metal widely used for nuclear energy and treating cancer.

It is also one of the world's poorest countries, receiving close to $2 billion a year in development assistance. This article discusses the sanctions imposed and how they affect the country.

When you read the content we share and it causes you to think of others in your life who would benefit from seeing it, please don’t hesitate to share it with them.

Aurie Wicks, CA, CPA, CFP Bram Houghton, CFA, CFP

Wealth Advisor Wealth Advisor

(403) 835 – 4785 (403) 690 – 9376

Aurie.Wicks@CIBC.com Bram.Houghton@CIBC.com

CIBC Private Wealth consists of services provided by CIBC and certain of its subsidiaries, including CIBC Wood Gundy, a division of CIBC World Markets Inc.

"CIBC Private Wealth" is a registered trademark of CIBC, used under license. "Wood Gundy" is a registered trademark of CIBC World Markets Inc.

If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and/or a spread between bid and ask prices if you purchase, sell or hold the securities referred to above. © CIBC World Markets Inc. 2023.

Related posts

Bram Houghton

October 14, 2025

Market Update - September 8th - October 10th, 2025

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read moreBram Houghton

September 10, 2025

Market Update - August 2025 Edition

Highlighting the key aspects of what we have seen in global markets and the economy over the last two weeks.

Read more