Adam Slumskie

March 10, 2026

The Domino Effect: Why Markets are Rattled (and Why They Recover)

If you’ve been watching the news lately, it’s hard to ignore the headlines. Conflict in the Middle East has once again pushed oil prices into the spotlight, and as a result, we’re seeing that familiar (but also unfamiliar as of late) wave of volatility across global stock markets.

At the Intrinsic Financial Group, we often remind our clients that the market is a forward-looking indicator, not a backward one. It doesn’t react to what is happening as much as it reacts to uncertainty about what might happen next. Right now, that uncertainty is centered on the "black gold" that powers the global economy.

The Domino Effect: Why Oil Matters to Your Portfolio

Why does a conflict thousands of miles away affect the price of a tech stock in California or a bank in Toronto? It’s a classic domino effect:

- The Supply Shock: War, or even the threat of it, creates a "geopolitical risk premium." If tankers can't move through the Strait of Hormuz or production facilities are at risk, the global supply of oil tightens.

- The Inflation Tax: Higher oil prices act like a hidden tax on everyone. It costs more to ship goods, more to fly planes, and more to fill up your car. This pushes inflation higher.

- The Central Bank Response: When inflation stays high, Central Banks (like the Bank of Canada and the Fed) are hesitant to lower interest rates. High rates for longer can cool the economy, which is what the stock market is currently "pricing in."

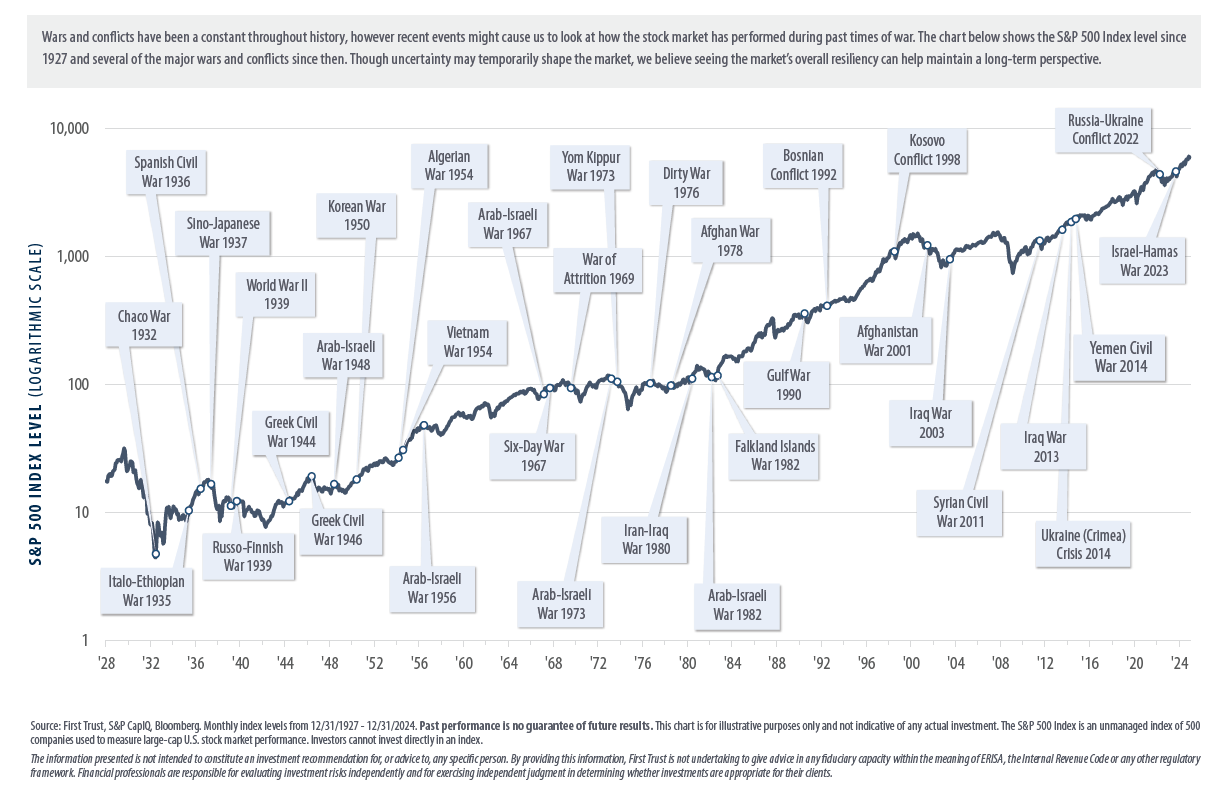

History is a Reassuring Teacher

It’s easy to feel like "this time is different”, but history tells a very consistent story. We’ve looked at 20 major military conflicts since WWII. On average, the S&P 500 falls about 6% during the initial shock, but it typically takes only 28 days to return to its pre-war levels.Even in more severe cases, like the 1990 Gulf War or the 2003 invasion of Iraq, the pattern holds. In 2003, markets fell initially, then rallied over 30% within the following twelve months.

Markets hate a vacuum of information; once the direction of a conflict becomes clearer, capital tends to flow back into equities with a vengeance.

If I’m finding an interesting point over the last week or so, it is the movement in gold prices. The argument for higher gold over the last year has partly been that the US dollar is no longer the safe haven and gold is taking its place. Given that rhetoric we would think gold would have surged over the last week but instead we’ve seen it fall around 8% and the US dollar rise. Just some food for thought there. It’s not a negative towards gold or commodities just maybe some insight as to current valuations.

The Path to Lower Prices

Many are wondering how the current administration will handle this. President Trump has historically campaigned on a "drill, baby, drill" platform, aiming for U.S. energy dominance to drive prices down. We have to remember that oil at these prices doesn’t help many people. It’s even tricky for producers as they hesitate to ramp up on something that could be short-term. That is being shown in oil stocks as many have barely moved over the last week despite the price spike. We’ve been underweight oil for 11 years but this could allow us an opportunity to dip our feet back in on the energy trade as a more normalized but higher price would be long-term beneficial for producers.

While Trump has acknowledged that war causes a short-term spike, his strategy is often focused on two things:

- Increasing Domestic Supply: By deregulating and encouraging record-breaking U.S. production, the goal is to flood the market, making it harder for geopolitical shocks to keep prices high.

- Declaring a "victory" for the consumer: Trump views low energy prices as a key metric of economic success. We expect the administration to use every lever from Strategic Petroleum Reserve releases to diplomatic pressure on OPEC, to ensure this spike is a "blip" rather than a trend. He wants to be the one to tell Americans (and the world) that he "fixed" the energy crisis. Surprise, surprise, as we’ve seen this playbook multiple times over his terms.

The Intrinsic Perspective: Where is the Opportunity?

When others are selling out of fear, we look for the intrinsic value that hasn't changed. The current dip is often a "sale" on high-quality companies that have nothing to do with the oil price but are being dragged down by the general market sentiment. Historically, buying when the "noise" is loudest has been a winning strategy. It’s not our first rodeo so to speak, and we know very well that although the volatility that we’re seeing in markets is not comfortable, discomfort can be an excellent set-up for future returns.

The Bottom Line: Don't let the headlines dictate your long-term plan. War creates volatility, but it rarely breaks the back of a strong economy. We remain focused on the data, stay disciplined in our rules-based approach, and look for the opportunities that uncertainty always leaves behind. As a final note, I want to mention that Canada has really surprised us as of late. Although locally we are certainly feeling the effects of tariffs, on a broader scale I’m very pleased with some of the strides made over the last 6 months or so. In my opinion, and I’ve said this often, the US will come back around to Canada and when it does, the setup on the Canadian side will be an interesting one, especially after a treacherous last 10 years in comparison to our neighbours to the south.