Milan Cacic

April 17, 2026

Money Economy Commentary Weekly update Weekly commentary

MARKETS ON MUTE: HEADLINES SCREAM AND STOCKS SHRUG

At the start of the year, none of us had “Venezuela regime change” or “war in the Middle East” on the bingo card. And yet, here we are.

Inflation is ticking higher again, largely driven by the knock-on effects of the war – mainly through energy prices. The issue isn’t roaring demand, it’s dwindling supply. Oil prices have moved higher, and that feeds straight into inflation. The problem is this isn’t the “good” kind of inflation that you can cool off with higher rates. You can’t hike your way to more oil. All higher rates do in this scenario is slow everything else down.

So, instead of the near, clean story markets were hoping for – inflation down, rate cuts in, smooth landing – we get something messier: inflation sticking around while growth starts to wobble. Not ideal.

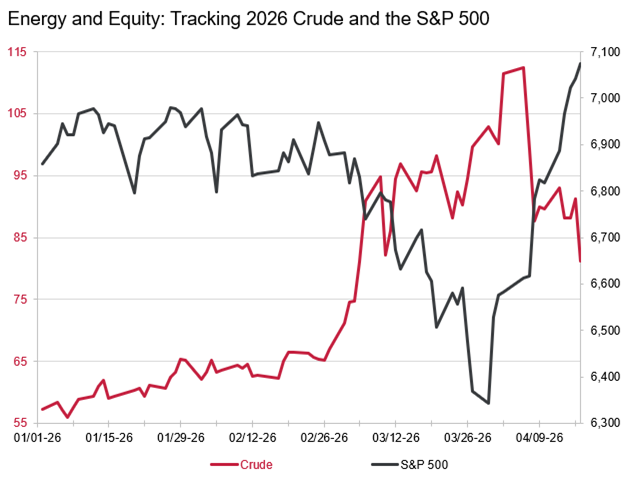

And yet... markets have been doing okay (if you’re in the right sectors). In fact, as you can see from the chart below, we’re back near all-time highs – which feels slightly odd given everything that’s going on. Part of that is markets looking through the headlines and assuming things will settle down. Part of it is that companies have quietly been getting on with it. Earnings have held up well, and plenty are still beating forecasts. While higher rates tend to push valuations down, stronger earnings have helped offset that. Add in the valuation reset we saw in tech earlier this year, and suddenly things look a bit more reasonable than they did a few months ago. In the background, AI spending continues to support both the economy and markets. That’s been a real tailwind, and it hasn’t gone away.

Source: LSEG [.SPX-UT and Light Crude CL/1-NM]. Data as of market open Apr 17, 2026.

In plain English: markets are holding up better than expected because expensive stocks came down and cheaper stocks went up.

It’s also worth nothing that this isn’t the easiest setup for more conservative investors. Bonds – usually the calm, steady part of the portfolio – don’t love a “higher for longer’ world. An increase in interest rates makes bonds go down, which is not great for the typical balanced portfolio.

Markets don’t move in straight lines, and they rarely follow our script (unfortunately). The story hasn’t broken; it’s just gotten a bit more confusing. Here’s hoping the next month brings some clarity.

I have also included a piece from our CIBC Economics team entitled “What to expect when you’re expecting expectations”.

As always, if you have any questions, please feel free to give us a call at any time.

Have a great weekend.

Milan