Milan Cacic

May 22, 2026

Money Financial literacy Economy Commentary In the news News Trending Weekly update Weekly commentary

DUELLING NARRATIVES: AI BOOM VS. YIELD GLOOM

The market has developed a bit of a Dr. Jekyll and Mr. Hyde personality lately.

On the Dr. Jekyll side, investors continue to cheer the AI boom. The world’s largest technology companies are spending hundreds of billions of dollars building data centers and AI infrastructure at a pace that resembles a government stimulus program more than normal corporate spending. Earnings growth remains strong, capital spending keeps rising, and the economy continues to benefit from the ripple effects.

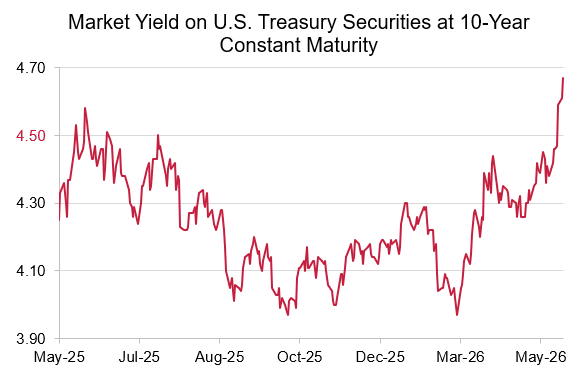

Then Mr. Hyde shows up holding a bond chart.

Source: Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS10], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS10, May 21, 2026.

The U.S. 10-year Treasury yield has quietly moved back above 4.5%, which historically has been a level where markets start to get uncomfortable. Higher yields create direct competition for stocks and pressure valuation multiples lower. Put simply, when investors can suddenly earn close to 5% in government bonds, they become less willing to pay 22x earnings for equities.

And that matters.

If yields continue toward 5%, valuation math alone could compress market multiples meaningfully, even if corporate earnings remain healthy. At the same time, oil and commodity markets are starting to flash inflation warnings again. Energy prices continue to rise while bond markets still seem relatively relaxed about inflation expectations, at least for now. That tension is what markets are wrestling with today.

One side sees an AI-driven productivity and earnings boom. The other sees structurally higher inflation, rising rates, and the possibility that central banks may not be cutting rates anytime soon. Put another way: one side of the market is busy buying Nvidia chips, while the other side is reading the inflation report with a bottle of antacids nearby.

In environments like this, diversification becomes increasingly important. Traditional stock and bond relationships have become less reliable, while hard assets, alternatives, commodities, and cash are beginning to matter again in portfolio construction. We have added hard assets, cash, and commodities to all our models.

I have also included a piece from our CIBC Economics team entitled “The squeeze from Treasuries”.

As always, if you have any questions, please feel free to give us a call at any time.

Have a great weekend

Milan