Corporate Earnings - The Market's Long-Term Driver

The stock market can exhibit volatility over the short term for a myriad of reasons: war, tariffs, pandemic, terrorism, oil price spikes, recession, inflation, natural disasters etc. Many investors who are focused on these short-term influences feel compelled to act, usually selling ‘until things settle down’. Translated this means selling at discounted prices until those prices go higher. Counter intuitive to say the least. Focusing on these often-dramatic short-term drives of stock prices and market panic makes it difficult to achieve success in capital markets. The big picture long term investor focuses largely on one thing – corporate earnings.

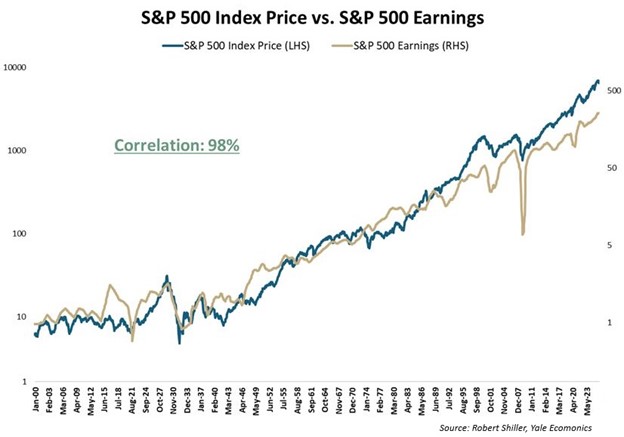

Over the long term, rising corporate earnings and rising stock markets are joined at the hip, but the path connecting the two is anything but straight. Investors often hope for a tidy picture where profits go up, share prices follow neatly along, and wealth compounds in a smooth, reassuring line. Reality is that price trends are closer to a messy scribble around that smooth earnings line: fundamentals quietly grind higher in the background while markets lurch ahead, stall, and occasionally go into reverse. The key is understanding that the long-term upward slope is driven by earnings; prices just oscillate around that trend.

Think of corporate earnings as the engine under the hood and stock prices as the speedometer on a winding road. Over decades, the engine’s horsepower derived from earnings does most of the work to determine how far and fast investors travel. Short term prices though are driven not only by that earnings engine, but also by the investor’s confidence and sometimes sheer emotion. In good times, investors floor the gas pedal, pushing valuations (P/E ratios) to levels that outpace actual earnings power. In tougher times, the same underlying businesses can trade at far lower multiples, even as profits continue to grow. The long-run result is intuitive: where earnings go over 20 or 30 years, prices eventually follow, but the ride is noisy and often uncomfortable.

The fundamentals are straightforward enough. Every share is a claim on a stream of future earnings, discounted back to today. Higher earnings and healthy reinvestment raise that stream; lower interest rates and risk premia increase the present value applied to it. When both are moving in your favour - growing profits and falling discount rates - you get periods of spectacular market returns and expanding multiples. When earnings march higher, but rates rise or risk appetites shrink, you can see the odd spectacle of “good” fundamental news paired with flat or even negative equity returns. This is why earnings alone, taken in isolation and over short horizons, can be such a poor comfort to investors watching their portfolios swing.

Investor psychology complicates things further. Many people implicitly believe the market should move like a flat line with gentle ripples: buy a stock, it ticks up, and any dip must mean something is “wrong.” The line investors should be watching is the earnings trend, which, for well-run companies and diversified indices, tends to slope upwards over time. Prices whip around that trend like a loose rope. Buying just before a drawdown feels like a mistake, even if the underlying earnings continue to compound quietly in the background. That disconnect is what leads investors to sell strong businesses after temporary price setbacks and sees them anchoring on previous “high water marks,” rather than recognizing that the real risk is not a 15% pullback around an upward trend, but owning businesses whose earnings power does not grow at all.

For patient investors, the implication is both simple and uncomfortable. Over the long haul, what you earn from equities comes down to three things: the rate at which aggregate earnings grow, the portion of those earnings paid out in dividends or reinvested wisely within the business, and the valuation multiple you pay going in versus what you receive going out. Growing earnings give you the slope of the line; valuation determines how far above or below that line you are at any point.

Think back to the long decline in interest rates from the early 1980s to the eve of the pandemic. The cost of capital fell for corporate borrowers, but the bigger story for equity investors was the steadily rising valuation anchor: as yields on safe government bonds moved from the teens toward zero, each dollar of earnings could be capitalized at a lower discount rate. Historical work on equity risk premia shows a strong inverse relationship here: high nominal and real rates tend to compress valuations, while low rates support elevated P/E ratios for extended periods. That is how you get long stretches where index prices compound faster than underlying earnings - investors are not just paying for higher profits, they are paying more for every dollar of those profits.

For long - term investors, the takeaway is to separate the durable from the transitory. Earnings growth is the durable piece - the upward - sloping line that wealth compounds along over decades. The hard work then is not only to own businesses whose earnings will be higher in five or ten years, but also to recognize when you are paying prices that already embed the full benefit of ultra-low rates and abundant liquidity. You must also be psychologically prepared for the day when those tailwinds turn into headwinds. The market will, in time, do what it always does: wander, overshoot, undershoot—and eventually converge back toward the steady, unglamorous upward march of corporate profits.

Related posts

Brady Clark Advisory Group

April 15, 2026

All We are Saying is Give War a Chance (or some time)

Geopolitical conflict always triggers the same instinctive questions about how investments will react. History provides some reassuring storylines.

Read more