Sneaky Bears and Falling Knives

Bear markets rarely begin with a dramatic signal. They often tend to sneak up on investors, especially when portfolios are immersed in a long-term bull market that has rallied beyond fair value to expensive levels. At first, everything appears stable. Bad news may cause prices to wobble, but confidence remains intact with investors having been lulled by the long-term bull market and its resilience to prior wobbles. Then, almost imperceptibly, the current picks up. Before you know it, you’re drifting down the river in your raft, and the distant roar of a waterfall starts to build. By the time you fully recognize the risk, it’s too late – the roar was in fact a bear.

In these conditions, the advice to ‘buy the dip’ can be dangerous. While this strategy tends to work well when you’re adding to an asset that offers good value made great by bear market action, if you’re adding to an expensive asset that just got slightly less expensive, you may be opening yourself up to accelerated losses - dips may just be the start of a long term repricing process.

The pessimistic side of ‘buy the dip’ is ‘Don’t try to catch a falling knife’ – used to ward off investors from buying into a falling market. Catching a knife by the blade would be unpleasant to say the least. The saying is a bit dim though as it assumes every falling asset is dangerous to add to because the price may get even lower. Perhaps if your time horizon was short term (months, or one or two years) this could be true. Bear markets on average have taken a year to finish their decline before turning back up and if you need your capital out in 6 months, buying in a bear market can be dangerous as it may not recover in time. Nobody should be buying stocks for the short term though.

If you’re investing for the long term (5+ years), even if your timing is terrible and you buy at the peak on the eve of the bear decline, you’ve historically been able to not only outlast the bear but to enjoy a few years of the next bull as well. Bull markets tend to last 5x as long as the bears and their upside tends to be 8x the bear that preceded them. The key to navigating difficult markets is understanding the investments you own and knowing whether you’re buying good value or an expensive trap. Think of buying good value as catching that falling knife by the handle. Still a bit tricky but not dangerous if you’re good at it. If you don’t know how to value a business, you don’t know which end is which and may grab the blade.

Consider shares of Microsoft in the year 2000. After hitting its all -time high December 27, 1999, Microsoft was the largest market capitalization company in America and traded for an exorbitant price at 69x its earnings for the previous 12 months – this is more than a 300% premium to the historical stock market average valuation of 16x earnings. By April 2000 as the tech bubble began showing signs of strain, the stock had fallen -20%. Many investors stepped in to ‘buy the dip’. It turned out they were in fact catching a falling knife because Microsoft was still expensive at over 50x earnings. The stock continued falling to early 2002, a further -60% decline for those April 2000 dip-buyers (knife-blade catchers as it turns out). It would take them 10 yrs just to break even, highlighting the danger of catching a falling knife.

Interestingly had you stepped in to buy Microsoft in at the start of 2002, you paid about 10x earnings for a world class growth business…a strong value buy by any measurement. You then watched your investment fall -20% over the next two months as the tech wreck and September 11th bear continued. Holding through with confidence was less of a challenge because if you did your homework, you knew Microsoft to be good value. If the 2002 buyer held through to today, their Microsoft is up 1800%. This highlights the wealth creation that can come from buying world class businesses at discounted prices and owning them for the long term.

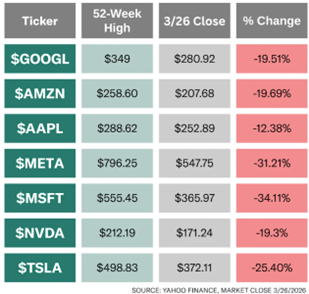

The last 6 months have again told the cautionary tale that owning expensive valuation securities can pose – Microsoft traded at roughly 35x earnings last fall, more than a 100% premium to that long term market valuation of 16x earnings. Concerns about AI advances threatening software businesses and the Iran war volatility have shone a spotlight on this overvaluation and the market has pulled the price back from $555 a share in October to $367 today in early April. As a result of this price action, Microsoft now trades at 22x earnings…getting closer to the long - term market average. Perhaps it will stray into value territory? If so we’ll be keen buyers.

The recent market declines have shifted a number of businesses that have been too expensive for us over the past 3 - 4 yrs into near value territory. This is the beauty of a market correction that most investors miss - the opportunity. As we sit today, most of the Magnificent 7 have been not so magnificent of late. As a group they’re all down -15% to -35% from their highs near the end of 2025. This while the rest of the market has been slightly positive.

A few of them are starting to edge closer to reasonable valuations, something investors may want to watch for.

Related posts

Brady Clark Advisory Group

April 15, 2026

All We are Saying is Give War a Chance (or some time)

Geopolitical conflict always triggers the same instinctive questions about how investments will react. History provides some reassuring storylines.

Read moreBrady Clark Advisory Group

May 01, 2026

Corporate Earnings - The Market's Long-Term Driver

Short-term stock market volatility tends to capture the most headlines. But is is really what has the biggest determinant on returns? Perhaps investors should focus on earnings in the stock market, as...

Read more