David Ricciardelli

April 27, 2026

Economy Commentary

War, What is it Good For

Since the end of February, we have spoken to many clients who have questions about the war, energy/fertilizers, the pullback in market, and (more recently) this bid for risk assets and how markets are back at an all-time high. I have little of substance to add on the war or the Strait of Hormuz, so I rely on trying to put today’s market in a historical context. I feel like a Farmers Almanac of market history. Here is what the last eight weeks have reinforced:

- We never know what markets are going to do in the short term,

- The benefits of being diversified, and

- The importance of staying invested.

The clients with the most challenging outcomes (so far) are the ones that have moved to cash, chased energy and fertilizers, or continue to sit on larger cash balances waiting for a lower entry point. These strategies may work out (see the first bullet), but we will try to put the current market backdrop into context.

War

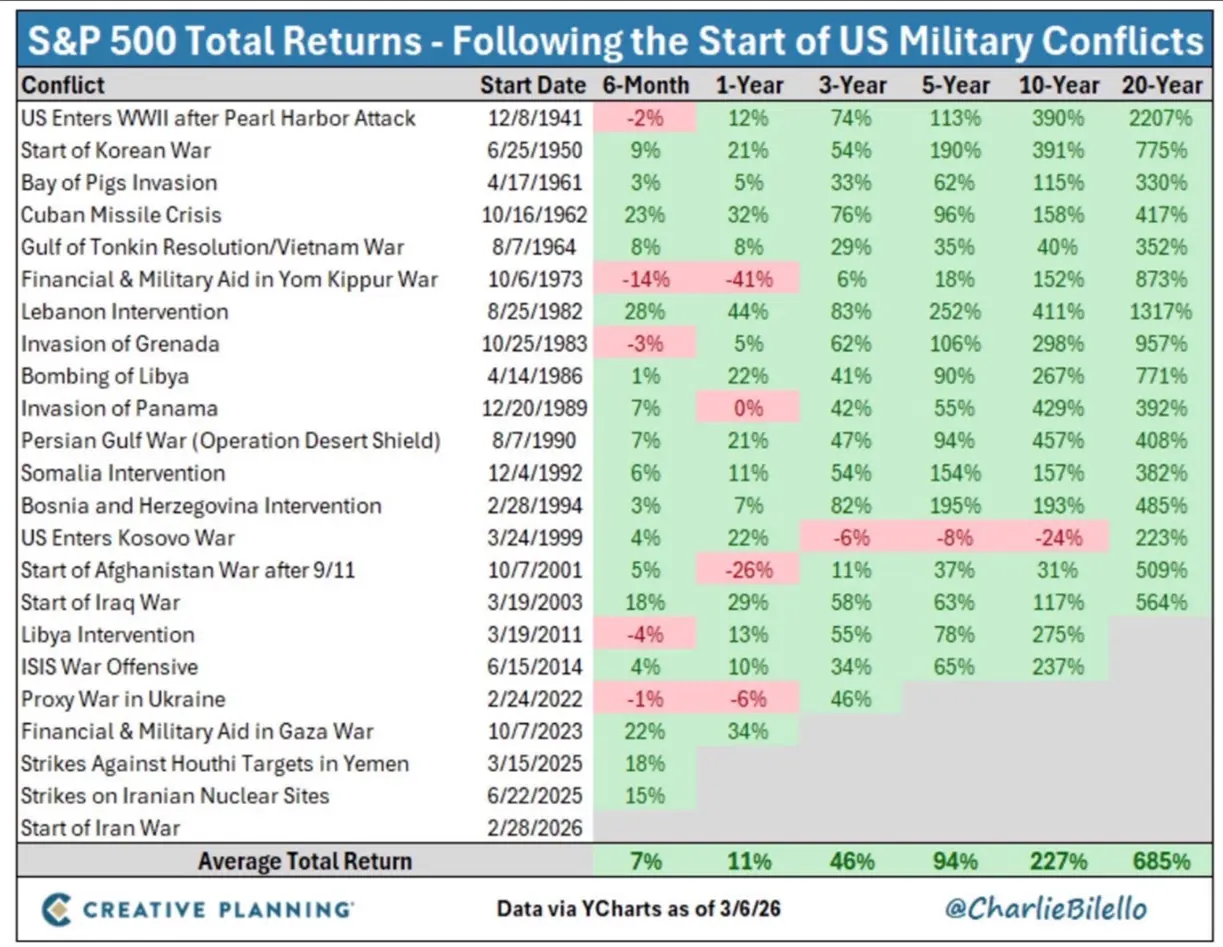

While war is terrible from a social, political, and humanitarian perspective, the impact on the S&P 500 tends to be more muted unless we have a protracted conflict. The table below shows the market’s reaction to major geopolitical events since 1941. The average drawdown is 5.0%, with the market recovering to pre-war levels in about 47-days. For context, the Iran War started on February 28th, the S&P 500 troughed on March 30th down 7.8%, and recovered back to pre-war levels on April 13th, 46 days later. You will also notice there is a lot of green in the table six-months after the start of a conflict.

There is Always a Reason to Sell

While there is always a reason to sell the market.

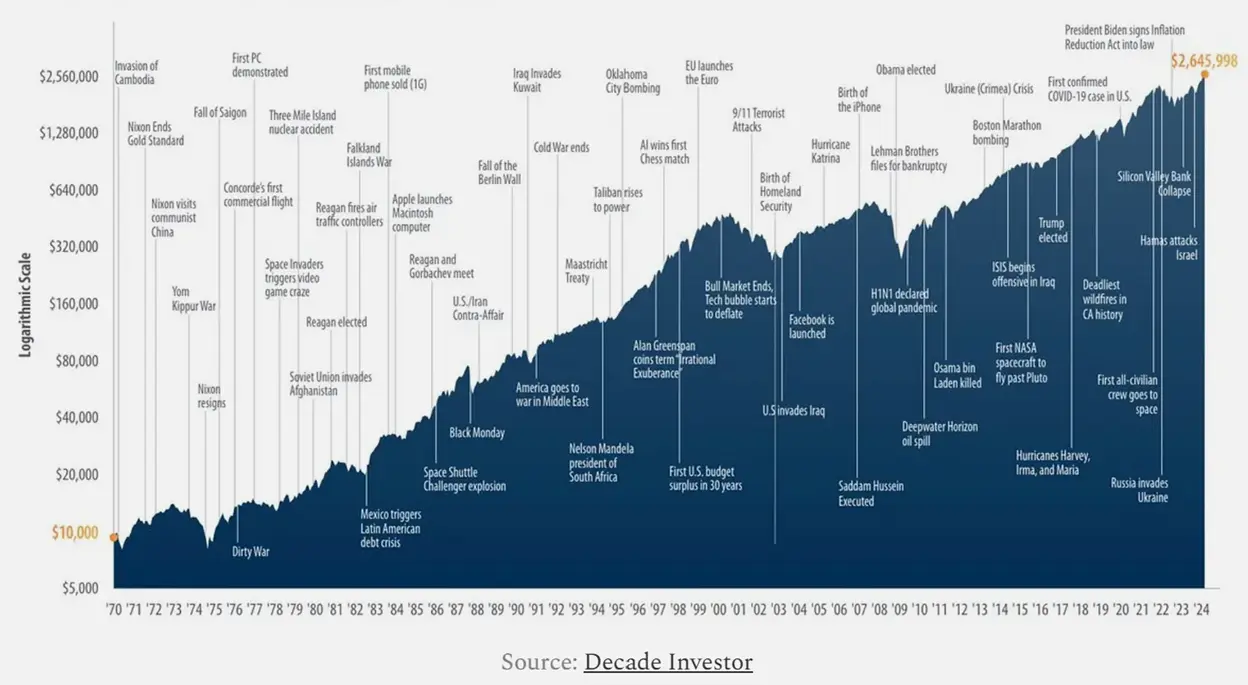

Crises Events Since 1970

Time Horizons Matter

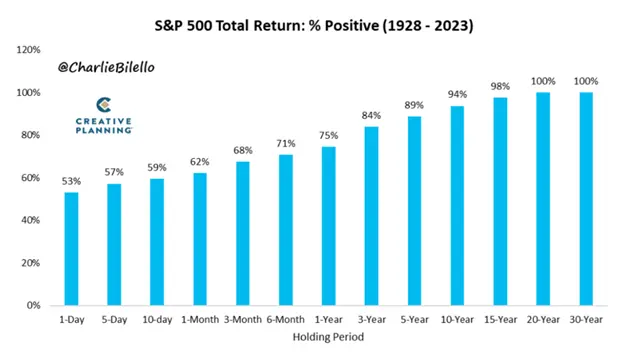

More important than timing the market is time in the market. Timing the market is very difficult. Staying invested isn’t easy but it’s easier to stick the landing. The chart below clearly shows that the probability of positive returns increases with time.

Invest as Soon as You Can

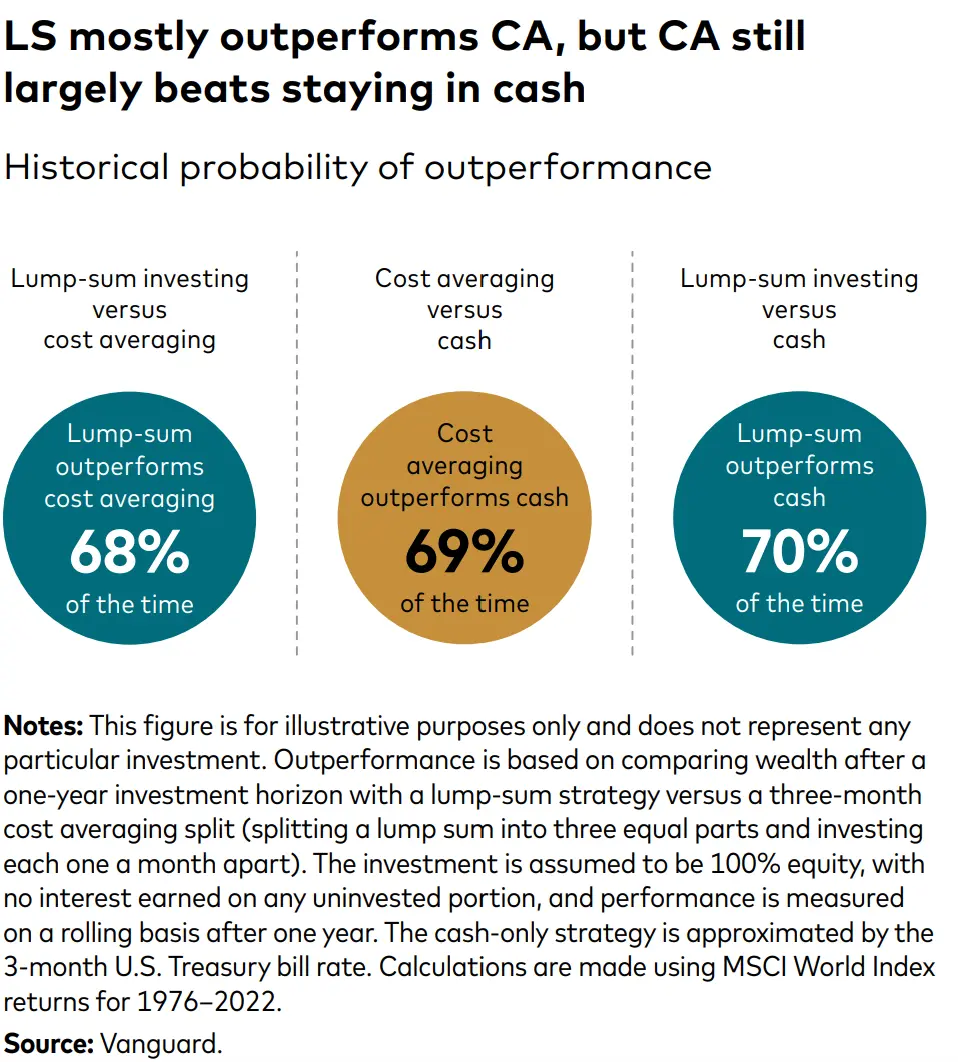

Since markets trend higher over time, it’s no surprise that an investor should try to get exposure to markets as soon as possible. This is the finding of a Vanguard Study (“Cost averaging: Invest now or temporarily hold your cash?”) that shows that investing a lump sum immediately has higher returns than investing portions of the same lump sum (which they call Cost Averaging) over time about 68% of the time.

The Most Important Driver for Markets

Earnings are the most important driver of market performance.

Earnings Have Been Stronger Than Expected

Through May 3rd (75% of index earnings reported), 74% of S&P 500 companies that have reported first quarter earnings that exceeded consensus expectations. Earnings are currently tracking up +17% higher year-over-year.

Valuation

In spite markets being at all-time highs, strong earnings have compressed valuation. The S&P 500 is at an all-time high despite the forward price-to-earnings multiple being 7% lower than where it was to start the year; it was down 15% at the end of March.

(Source: Bloomberg)

Forward price-to-earnings multiples have compressed most in the technology sector. We haven’t seen tech valuations in this range since the technology bear market in 2022.

What's an investor to do?

The key for investors is often to stay invested and diversified. There are always reasons to sell, but you will not find many investors happy about selling in 2018, 2020, 2022, or in early 2025, when the market was down 19%. In 2025, and early 2026, the key (again) was to stay invested.

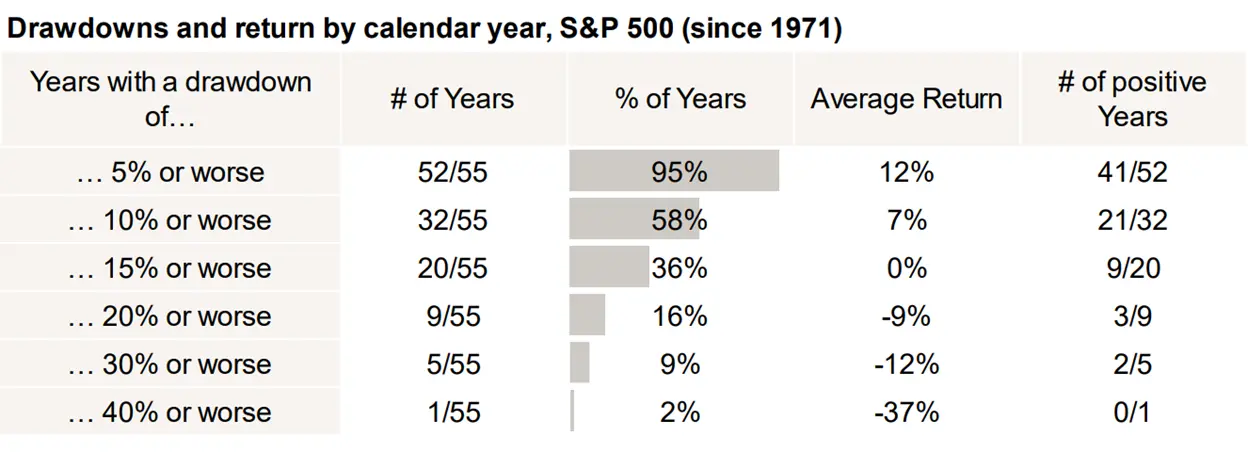

As investors, the ‘price’ we pay for returns is gut churning volatility. The table below shows the probability of 5% to 40% pullbacks for the S&P 500 each year. The volatility we are currently experiencing is normal. It could get worse and still be normal.

While action helps alleviate anxiety, timing markets is extremely difficult. Investors will benefit from saving and investing consistently across market cycles. This process allows investors to buy more securities when the market is inexpensive and fewer securities when the market is expensive. Consistently investing across market cycles also provides investors with fresh capital to exploit emerging structural changes.

Some investors may find value in a barbell strategy, where high-quality companies exposed to secular themes provide equity market exposure. The other side of the barbell is cash, actively managed fixed income and alternative investments that may reduce volatility and provide ballast for portfolios. For investors in the distribution phase of their lives, the focus expands to optimize the tax efficiency of distributions.

Don't hesitate to get in touch with me for a more detailed discussion.

Delli (delli@cibc.com)

Disclaimers:

This information, including any opinion, is based on various sources believed to be reliable, but its accuracy cannot be guaranteed and is subject to change. CIBC and CIBC World Markets Inc., their affiliates, directors, officers, and employees may buy, sell, or hold a position in securities of a company mentioned herein, its affiliates or subsidiaries, and may also perform financial advisory services, investment banking or other services for, or have lending or other credit relationships with the same. CIBC World Markets Inc. and its representatives will receive sales commissions and a spread between the bid and ask prices if you purchase, sell, or hold the securities referred to above. © CIBC World Markets Inc. 2026.

Commissions, trailing commissions, management fees, and expenses may all be associated with hedge fund investments. Hedge funds may be sold by Prospectus to the general public, but more often are sold by Offering Memorandum to those investors who meet certain eligibility or minimum purchase requirements. An Offering Memorandum is not required in some jurisdictions. The Prospectus or Offering Memorandum contains important information about hedge funds - you should obtain a copy and read it before making an investment decision. Hedge funds are not guaranteed. Their value changes frequently, and past performance may not be repeated. Hedge funds are for sophisticated investors only.

If you are currently a CIBC Wood Gundy client, please contact your Investment Advisor.

Related posts

David Ricciardelli

October 10, 2023

Tis the Season for Market Rallies?

As the leaves change we try to put investor sentiment, seasonality, equity and fixed income markets, and soft landings into context.

Read moreDavid Ricciardelli

August 22, 2022

Charts for the Lake

Some thought provoking charts that examine markets, recessions, capital spending and summertime rallies.

Read more