Andrew Lacas

January 04, 2024

Happy New Year! 2023 - A Year in Review

Another year comes to a close and what a year it was. Inflation continues to run at decades high levels, interest rates at levels not seen in over a decade, credit card debt at all time highs and record low consumer savings rates, yet the S&P 500 is trading at the time of this writing within a few points from it’s all time highs. It has been a difficult two years to navigate as an investor so I wanted to take some time to discuss some high level thoughts, share some successes and also where we are improving. Before we get into our models and what we’re doing on the team I thought I would share some interesting comments about the condition of the markets, then two macro comments, one bearish and one bullish.

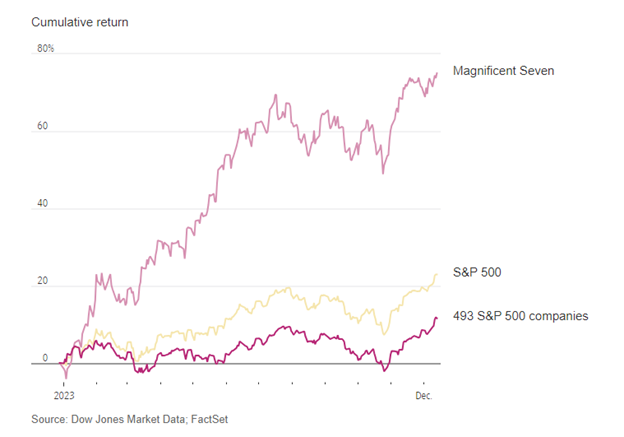

But first it has been the tale of two very distinct markets this year. On one hand you have the “Marvelous 7” which is made up of Amazon, Google, Apple, Microsoft, Tesla, Nvdia, and Meta. As we approach the end of the year they have made up roughly 65% of the S&P 500 return and now account for over 30% of the market cap.

We have seen concentration in markets in the past. In the late 90’s with the dot com bubble concentrated in telecom and tech and in the early 70’s with the “nifty fifty” as two examples. The past tells us whenever you have such a concentration that sooner or later the markets will revert back to their mean. The extreme concentration in the marvelous seven is beyond anything experienced in the markets.

In past letters we’ve discussed the increased use of passive investments which removes a lot of fundamental decision making and we feel continues to add to the concentration risk. The US markets account for 62% of the global market cap. The magnificent seven account for over 30% of that. So for every dollar that gets added to passive ETFs a significant share flows to those seven companies regardless of their fundamentals. I want to be clear though, we are not saying that those companies are bad companies. In fact we do still own a couple of them, albeit at lower weights. On the flip side of the coin we’ve also seen companies have very challenging years. As recently as Oct 2023 we saw the like of CIBC and BNS trading at roughly 16 year lows and BCE down 25%. According to Tier1 Alpha, on Dec 31st 2023 50% of the S&P 500 were still down over 20% from their 2021 highs and 27% are still in “crash” mode down over 30% from those highs. Clearly it it isn’t puppies and rainbows for everyone.

One of the most interesting and challenging things that have taken hold in 2023 has been the rapid growth in 0DTEs. This stands for zero days to expiry options. In a nutshell, an 0DTE is a call or put option that expires within 7 hrs. Let’s say company X is currently trading at $9.50 and you buy a call option in company x at a strike price of $10. Let’s say that the option costs you 25 cents. What this means is that you need company X to end the day at $10.25 for you to make money. Anything less the $10 and your option expires worthless. With a 0DTE call option you are essentially making an “all or nothing” bet that the market is going to end the day above your strike price and with a put option you are betting the opposite direction. Now making these type of bets are the antithesis of long term investing as nobody knows what will happen in a given day in the markets. What is fascinating however, is the sheer volume that is being invested in these options. As an example on Friday Dec 15th there was over $3.1Trillion of notional value call options expiring that day. That is almost 9% of the total market cap of the S&P 500. In the short term, investing with markets that are being impacted by these types of transactions can be extremely challenging and frustrating, but we do believe that fundamentals for companies or economies eventually determines prices.

This year also surprised with robust non-farm payroll numbers. The market has taken these numbers and ran with them, but we thought it would be prudent to delve a little deeper into them. According to our friends at Hedgeye, who dig into more numbers then any research team I’ve seen, employment numbers might not be rosy as they first appear. First and foremost the NFP numbers have been revised down for the last eight months and counting. Previous times we have had revisions like this have been the dot com bust and GFC. Why this happens is that there is an aspect of the non-farm payroll numbers that is called death and birth numbers. Basically there is an assumption that a certain amount of jobs disappear and also are created in any given month. Later on though those assumptions turn into reality and the numbers are revised either higher of lower depending on reality. Unfortunately they continue to get revised lower. Consider overtime hours, going back to 1988.They are currently at the lowest levels they’ve been other then during the Great Financial Crises and the heart of the COVID crises. Year over year growth in temp staffing has decreased to the lowest levels since the dot com bust, the GFC and COVID. This does not mean that we are suggesting a GFC or COVID style market collapse as the situations are not the same, but we do suggest that some prudence is warranted as these are not factors that positively affect the economy.

On the positive side of the ledger, interest rates are getting close to pivoting. In fact the markets are now pricing in 6 rate cuts for 2024. We believe that might be a tad aggressive and the Fed is

guiding to 3 rate cuts. Historically the Fed and the markets haven’t quite nailed the pace of change, the most recent example being “transitory inflation” in 2021. Nobody was pricing in rates to be where they are now. That being said, it is pretty clear that we are at the top end of the range. This is bullish for both bonds in general and interest rate sensitive companies like utilities, pipelines and real estate to name three categories. As rates flat line and then eventually come down a bit, those rate sensitive asset classes benefit for two reasons. One their yields start to look attractive again, and also because they tend to carry significant debt and therefore that debt becomes easier for them to service and manage. This bodes well for the back half of 2024 in our dividend portfolios. History has shown us that although rates decreasing is indeed positive for interest sensitive companies it also has been the trigger for a correction in the general market. This is a historic reference that re-enforces our positioning with cash, bonds, utilities and gold.

Moving onto your portfolios. First and foremost we believe our job is to steward your hard earned capital and avoid unnecessary downside. This means that we will not chase asset classes that have run hard and we are much more patient with our purchases. We are firm believers that we can go anywhere to invest for the best risk adjusted return potential but that doesn’t mean we will go everywhere. One thing we have talked about with many of you over the past few months is our concept of “north star” investing. What this means is focusing on what is important to you and your family. Truly understanding what your goals are and how we can generate the cash flow to achieve those goals with the least amount of risk possible. It is not what is market x or company y doing. It is are we achieving your specific goals. The best way to truly figure out these short and long term goals is to develop a financial plan, so if you haven’t taken us up on the offer to get a plan in place then I highly urge you to reach out to Caroline to set a time in 2024 to go through the steps. We will continue to speak to all of you about this as well. Once we’ve figured out what that “north star” is, then we need to develop the investment plan to match it, and that’s where the different model portfolios come into play, so I wanted to take a moment to discuss a couple of them, but first let’s look at how different goals can be achieved.

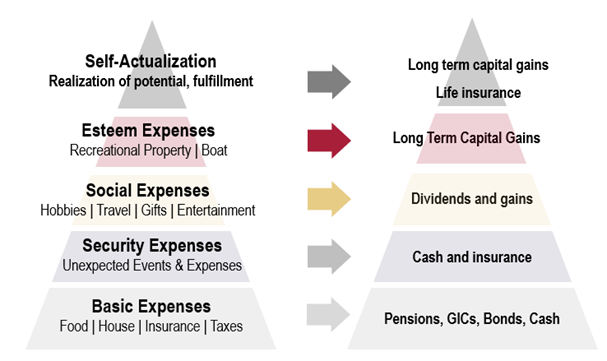

On the below chart that I put together, you’ll see on the left a version of Maslow’s hierarchy of needs. On the right I’ve associated it to a cash flow plan. When your north star is defined and a financial plan is created we have a path on how best to access your funds from a tax and estate planning standpoint. The next step is deciding on proper asset allocation and location. In order to achieve this goal we match your cash flow needs with the tranches of the pyramid below by using different asset classes and portfolios that will behave quite differently from each other. For each and every one of us this is a unique and customized approach.

I wanted to take some time to discuss our North American Core model and our Alpha model and how they relate to this pyramid. Our North American Core (NAC) model is exactly what the name implies. A portfolio of solid blue chip North American dividend focused companies and ETFs. Our primary goal in this mandate is to generate solid cash flow through dividends no matter the market conditions. These dividends can then be used to cover all those “social” or lifestyle expenses. These are the expenses that make life more enjoyable. This portfolio has done its job. Although it has had some underperformance versus its benchmark in 2020 and in 2023 as growth (ie. non dividend names) have led the charge it has outperformed in the strong bull market of 2021 and had a huge beat in 2022. More importantly when we look at NAC through the context of creating a steady and dependable cash flow for you we are now generating roughly 4.5% of annual cash flow while still having a defensive positioning of roughly 13% in high interest savings. We are very comfortable with the current positioning and how this portfolio has been running and it is serving its purpose for that portion of your allocation.

Our Alpha portfolio is more of a go anywhere, but not everywhere strategy. It did extremely well in 2020, 2021 and most of 2022, but has underperformed the last 15 months. This portfolio is focused more on the social and esteem expenses and in some cases the self-actualization stage. Our biggest mistake in this portfolio has been timing on two asset themes. The first is we were too early buying two companies in the metals space. Albemarle and MP Materials are industry leaders in lithium and rare earths. We believe these critical minerals will play a huge part in the energy revolution that is underway but unfortunately we were too early. Although we bought initial positions significantly off their respective highs, those buys were too early, as their underlying commodities subsequently had larger corrections. Both companies lead their respective space and are now trading at very depressed multiples so we have been taking advantage of the tax loss selling to add to the names. The other place we were wrong this year was in our trading of our smaller positions in VIXY and PSQ. PSQ is a short Nasdaq position and VIXY is a volatility position. Clearly as you saw from the opening thoughts of this letter, tech has led the charge this year so having some negative exposure to this sector has not helped us in the least. We have sold off some of this position and will continue to look for opportunities to exit completely over time. The VIXY position was put in place to protect against any potential shocks in the system that create spikes in volatility. As an example in March when the US banks had their credit crunch we would have expected that volatility would spike like it has in almost every other crises. What we got wrong was just how much of an impact the 0DTEs have on volatility. Because of the massive amount of short term trading this has dampened short term volatility. It acts like your pushing a ball to keep it underwater. Although we have been hurt in this position this year, it is relatively small and we do feel that going into the beginning of 2024 we still want to maintain it and look for opportunities to reduce and exit completely. Although each of these positions on their own have not been huge they have attributed to a large percentage of the underperformance. On the right side of the ledger we have benefited massively from our uranium purchases, specifically Cameco where we have almost a 100% gain and have been taking profits off the table. We have also done well with our trading in energy. As an example at the beginning of the year we added almost 50% to our Arc Resources pick at $16 and sold it at different points throughout the year between $20 and $23. So what are we doing to minimize the mistake and maximize the wins?

I have taken the steps to invest quite heavily in a new research platform. It is a team that we have followed for two years and have been extremely impressed with the depth and quality of their research. This fall they rolled out a new institutional grade platform that we believe will help alleviate the types of mistakes that I alluded to above. With the help of their team we are focusing on return potential over 12-36 month tail durations. The team is providing us in depth research that lays out probabilities of either positive or negative returns in different companies, sectors and geographies over a 12 month window. What you are starting to see are allocations to sectors and geographies through ETFs where we feel we are taking a reasonable amount of risk to generate a reasonable rate of return. As an example we have recently initiated positions in US Aerospace and Defense, India, Japan and Emerging Markets ex China. Those three regions are all showing acceleration in expected growth over the coming quarters and in Japan’s case long term it has had significant structural changes that bode very well. Why we chose EM ex China is that China is becoming increasingly hard to invest in. There is increased geopolitical risk as well as the reality that their economy is decelerating. We believe that this additional research that we have invested quite heavily in will help us achieve those long term goals that will help fund the social and esteem expenses as well as the self-actualization.

The above portfolios are of course enhanced and augmented by the use of our partners at Walter Scott, Wasatch, Barrantagh, Turtle Creek and others depending on your specific needs.

In closing, although it has been a challenging year we are excited about the strides we continue to make and the investments in our business to continue to help you, our clients reach your goals. Although there will continue to be noise in the markets over the coming months and quarters we have never been more confident that we continue to develop the right structure and process to deliver the utmost service to you all. If you haven’t already availed yourself to our financial planning team then please reach out so that we can get one up and running in early 2024, it’s our goal to have 75% of you with a fluid plan in place that will help us create a path to follow your north star. Here’s to closing the chapter on 2023 and to all the future has to offer.

All the best,