Peter White

March 23, 2026

Market and Geopolitical Insights: Navigating the Iran Conflict

It has been a fluid few weeks as the markets have reacted to the potential short- and long-term implications of the ongoing conflict in Iran and the Middle East. While the loss of life, the level of destruction, and sabre-rattling from combatants with access to nuclear weapons is distressing to us all, market participants focus on the cold, hard facts: how will the de facto closing of the Strait of Hormuz impact the global economy? The clear and present danger is another jump in oil prices at a time where the global economy has recovered from the energy shock that followed the onset of the Russia-Ukraine conflict, and the inflationary implications of the tariff agenda being pursued by the U.S.

Since the conflict began, investors have weighed the odds of a quick cessation in hostilities against the risks of a larger regional conflict. After a few weeks of escalation, investors interpreted Trump’s statement on Monday morning that he plans to hold off on strikes against Iranian power infrastructure as a sign that the U.S. was seeking an off-ramp rather than an escalation. The Dow surged over 1000 points on the news. Whether productive conversations with Iran were held or not is up for debate, but investors are hoping talks move in the right direction to reverse the existing economic fallout. CIBC hosted a webcast last week where U.S. Admiral Stavridis, the Commander of U.S. Southern Command from 2006 – 2009, and the Supreme Allied Commander of NATO from 2009 – 2013, shared his perspective on the ongoing conflict involving Iran. The replay is available here, but we’ve summarized the key takeaways from that call, as well as market responses, and our current positioning below.

Geopolitical Overview: The Iran Conflict

The U.S. administration has been vague by design about its goals in the current operation against Iran. Whether the primary goal is regime change, decapitation of leadership, degrading Iran’s military, or destroying nuclear facilities remains unclear. This ambiguity allows the administration flexibility in declaring victory and shifting focus back to domestic issues, especially with the U.S. mid-term election cycle underway following the Illinois State primary on March 17th.

The early stages of the conflict underscore the vast asymmetry in military strength: the U.S. defense budget is 125 times larger than Iran’s, and the U.S. enjoys superior air and naval power, as well as regional allies. This dynamic suggests that hostilities are likely to end on U.S. terms, though the risk is that Iran continues to disrupt freighter traffic until that occurs.

With 20% of global oil supply passing through the Strait of Hormuz, Gulf nations (UAE, Qatar, Iraq, Kuwait, and Saudi Arabia) are facing storage constraints that could force production cuts. U.S. gasoline prices have returned to August 2024 levels, making affordability a hot-button issue ahead of the mid-terms and providing a strong incentive for a rapid resolution.

Reactions So Far

Central Banks

As Avery Shenfeld writes about in his recent posting (found here) Powell isn’t going to want to make any clear promises about further interest rate relief. CIBC economics had forecast two quarter point rate cuts in June and July, but given the energy price surge, our economists are pushing those cuts back to September and October, and that’s on the assumption that oil prices will have reversed the bulk of their run-up by the end of the summer. At this point in time, neither the Bank of Canada nor the U.S. Federal Reserve are willing to make any confident bets on how or when the conflict will be resolved.

Bonds

Bond markets have remained relatively calm but are pricing in more persistent inflationary pressures. U.S. long-term yields are at 4.4% (up 0.45% since March 1), and short-term yields are at 3.8% (up 0.4%), leaving the yield curve largely unchanged, but increasing borrowing costs. An inverted curve or long yields above 5% would be more concerning, but that’s not the case. Credit markets are not signaling distress. Corporate bond spreads, which typically widen during periods of uncertainty, remain stable and below long-term averages.

Equities

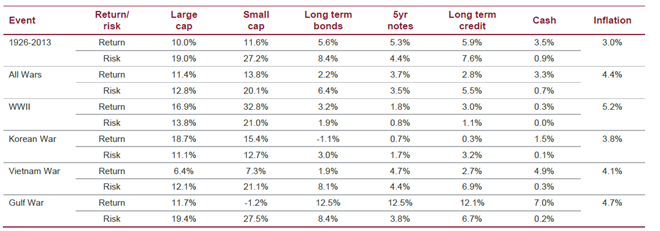

Stock market corrections due to armed conflicts have historically been muted and short-lived. Currently, U.S. markets are down 5% from their highs, and Canadian/global stocks are off 8–10%—well within historical norms. Sectors such as energy, infrastructure, utilities, and secular growth (AI infrastructure, hyperscalers) have outperformed, while cyclicals (consumer goods, industrials) have lagged. Notably, gold and healthcare, traditional safe havens, have also come under pressure, contributing to the underperformance of Canadian equities.

Chart showing risk and return profile of underlying market during periods of conflict

Positioning and Outlook

Investors could see ongoing volatility as the market digests oil supply risks ($120–$150/barrel oil would be a major headwind). However, the political and economic incentives for a quick resolution are strong. Despite headwinds, global markets remain positive year over year, supported by robust monetary and fiscal policies.

North American Stock Highlights

Secular Growers Outperforming: Stocks like Amazon and Microsoft, as well as software companies that were viewed as being disrupted by AI like Salesforce, Intuit and Uber, have rebounded sharply from oversold levels. Amazon is now at its lowest valuation since the Global Financial Crisis of 2008 (10x EBITDA), and Microsoft since 2018 (12x EBITDA).

Defensive Allocations: In income-oriented portfolios, investors can look to maintain higher allocations to utilities, infrastructure, and energy, alongside conservative tech names, which has supported relative performance.

Geographic Preferences

EAFE and Emerging Markets: These regions have outperformed year to date and are seen by investors as attractive given the valuations. While both regions are more sensitive to oil prices, many core countries (eg. China, India) have existing trading relationships with Iran and the U.S., which may insulate them from the conflict.

Global Infrastructure: A Standout Performer

Defensive Characteristics: Infrastructure assets such as utilities, transportation, and energy provide essential services making them less sensitive to economic cycles, potentially delivering more stable and predictable cash flows. Infrastructure assets track inflation well, preserving real returns over time. If high oil prices persist, this asset class should perform relatively well.

Final Thoughts

While the situation remains fluid, our disciplined approach and long-term conviction in high-quality, strategically positioned assets enable us to navigate uncertainty and capitalize on opportunities as they arise. We continue to monitor developments closely and will adjust our positioning as new information emerges.