Calvin T and Peter W

April 29, 2026

Market Insights from the Greenwood White Group

Markets have roared back to reach new highs over the past few weeks after a 10% price decline and 19% valuation drawdown prompted by the conflict in the Middle East (Fidelity). The AI related sectors have led during the recovery as the “Magnificent 7” regained their dominance. As financial markets seem to be shrugging off the geopolitical turmoil, this posting addresses whether participants have declared victory too early, and how we can diversify our portfolios to be prepared for the remainder of the year.

Diversification Remains Key

Diversification is a well-worn, but often misunderstood term in the investment industry. Modern portfolio theory is predicated on the thesis that not all assets move together. Correlation is a fancy word for the “co-movement” between two sets of assets – how much they move in tandem with one another in response to world and market events. The higher the correlation, the more the two assets move in tandem; negative correlation means the two assets move in opposite directions to world or market events. This forms the building blocks of diversification’s role in a portfolio: the lower correlation between your holdings, the more risk (or volatility) you eliminate without sacrificing return.

The challenge with this theory is that correlations are not stable. Two assets that are uncorrelated 90% of the time can become highly correlated when forced liquidation occurs in the market. Sometimes this can occur for unpredictable reasons. For example, in March, gold, which typically exhibits price stability during periods of distress (a “store of value”) was used as a source of cash by the central banks of nations most impacted by the closing of the Strait of Hormuz. In short, these banks were looking to create liquidity to fund their operations during the expected disruptions caused by this event.

Below is a list of the price correlations for several sets of assets during the month of March.

-

- Stocks & bonds = positive

- Gold & bonds = positive

- Dollar & Bitcoin = positive

- Stocks & crude oil = negative

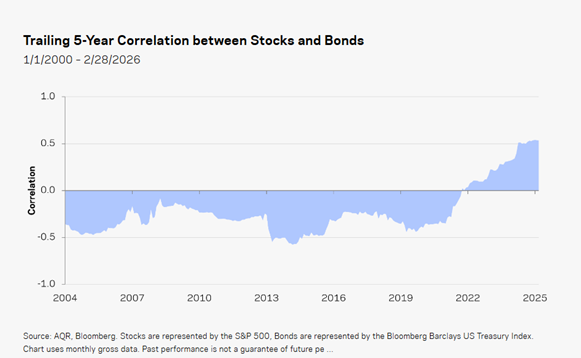

The most interesting is the relationship between stocks and bonds, which make up the majority of client portfolios. The correlation between stocks and bonds became positive a few years ago after decades of acting as proper diversifier (See figure 1). Although there are many theories as to why this is the case we tend to agree with the thesis put forth by Cliff Asness, co-founder of AQR Capital Management. Put very simply, his research suggests that stocks and bonds move together in environments where inflation expectations are uncertain. Neither asset likes high levels of inflation as earnings are lower for companies and the bond market fears rate hikes by central banks. On the contrary, growth news tends to move them in opposite directions. Stock prices move higher (in anticipation of higher earnings) and bonds are often sold as a source of cash to fund higher risk assets. Therefore, if inflation expectations stabilize again, we would expect a return to a negative correlation. Our view is that the recent energy supply shock raises the risk that volatility in inflation expectations persist, causing the positive correlation between stocks and bonds to persist.

How we are positioned

This has a clear impact on portfolio construction, and our solution since volatility in inflation expectations began to rise after the Ukraine crisis in 2022 has been, where practical, to increase weights in real assets like infrastructure, gold and energy, and maintain our weights in commodities, improving the defensiveness of our clients’ investments. By its nature, infrastructure is a defensive asset class. The revenues from these assets (toll roads, airports, pipelines, utility networks) are shielded by government contracts, long term agreements, and consistent fee streams making these companies less sensitive to economic shifts. The consistent demand through economic cycles translates to smoother earnings variability and price volatility.

A note on underlying earnings

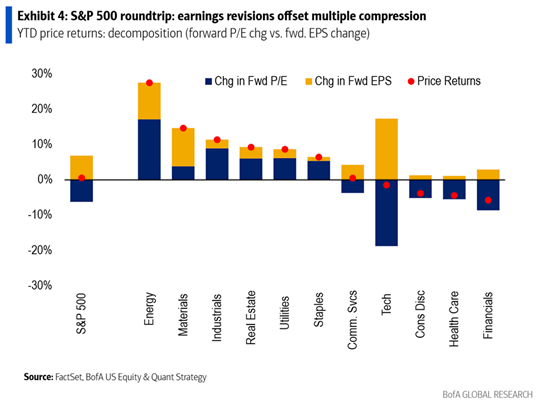

Despite the noise, the strongest support for markets continues to be robust fundamentals (see figure 2). YTD all eleven sectors have experienced positive change in forward EPS, with industry declines stemming from valuation compression.

As a result, we believe equities remain attractive given the underlying fundamentals. However, there are still risks to watch. Markets are still pricing in a quick conflict resolution, and the positive correlation between stocks and bonds continues to pose a hedging challenge (as discussed above). While the correlation between bonds moved higher in March, they are nowhere close to being perfectly correlated with stocks, and hence still add diversification benefits while generating predictable income.

We continue to believe the best course of action is to lean into volatility as a rebalancing opportunity, and not a risk event. There are opportunities available for those who are willing to be the providers of liquidity instead of following the crowds. We, and the managers we hire on your behalf, are focusing on companies that have had valuation compression rather than price declines for more reliable buy signals. Lastly, our focus on company fundamentals, and earnings growth remains paramount.