Greenwood White Group

June 05, 2026

Mid-Year Update

After the markets roared back in April, May remained steady as investors continued to factor in the de-escalation in the Middle East. Although negotiations remain ongoing and the administrations' decisions are difficult to predict, we share the market view that the likelihood of resolving the conflict is significantly higher than it was in March.

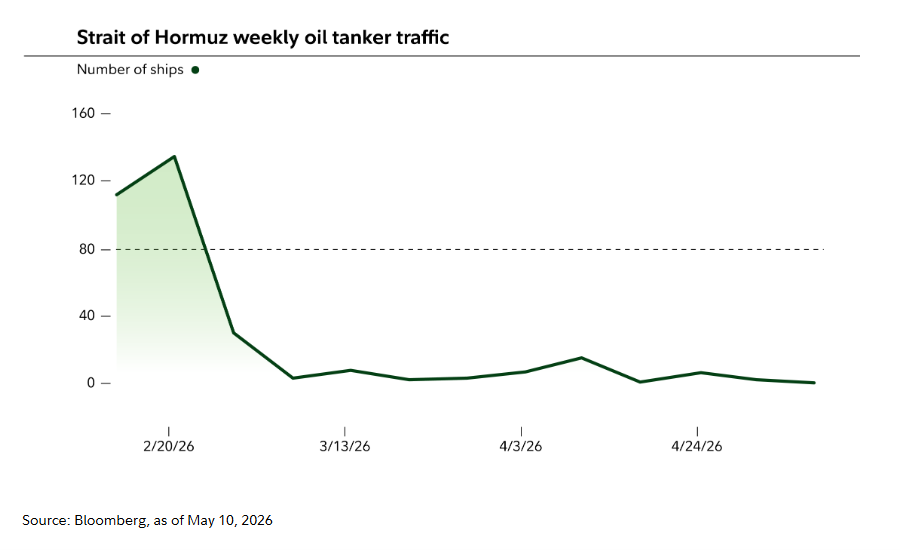

Negotiations have led to falling energy prices, but gas prices will only normalize once operations in the Strait of Hormuz are restored. Recent data shows oil tanker traffic through the Strait has dropped by over 90% from pre-war levels, suggesting it may take months for oil markets to stabilize (source: Bloomberg). Energy prices are likely to stay elevated for the remainder of the Trump Administration and central bankers across the globe must consider the risk of sustained higher oil prices when planning their next moves.

The Bull Case

In May, equities recorded another positive month. Growth equity returns (+7.0%) continued its outperformance over Value stocks (+2.3%). While developed markets continued a positive trend and closed the month higher (+4.6%), emerging markets outperformed other asset classes (+9.7%), led by extraordinary returns for Korea and Taiwan. These equity markets continued to benefit from their positioning in the AI supply chain and hyperscale-led investment demand (source: JP Morgan). If market bubbles are defined by excessive valuations and weak earnings growth, current conditions do not meet that definition. Companies are not only beating estimates; but they’ve also far exceeded them. As of May 11, 453 companies in the S&P500 had reported first-quarter earnings, with 84% surpassing analysts’ profit estimates (Fidelity). Strong fundamentals have supported equity markets, which continue to register low volatility, despite the uncertain geopolitical context.

The Bear Case

Oil markets may be more stressed than investors realize. If the oil supply shock lasts longer than expectations and energy prices remain at a premium, it will likely move equities lower, push bond yields higher, and restart inflationary pressures. Though the rate of inflation had settled at 3%, down from a COVID-fueled spike of 9%, this means future consumer price increases would start from a higher base. This would greatly impact the Federal Reserve's ability to deliver interest rate cuts before the end of the year.

Final Thoughts

De-escalation is supportive for both stock and bonds. However, equities have remained notably optimistic throughout the crisis, and in our view have already priced in a favorable outcome. Although political turmoil drives a ‘wider than normal’ range of return outcomes, risk assets (specifically growth stocks) are supported by both strong macro conditions and earnings growth, which are reinforced by a powerful AI-driven capex cycle. We continue to advocate for a diversified portfolio to mitigate single sector risks